Concept explainers

Videos

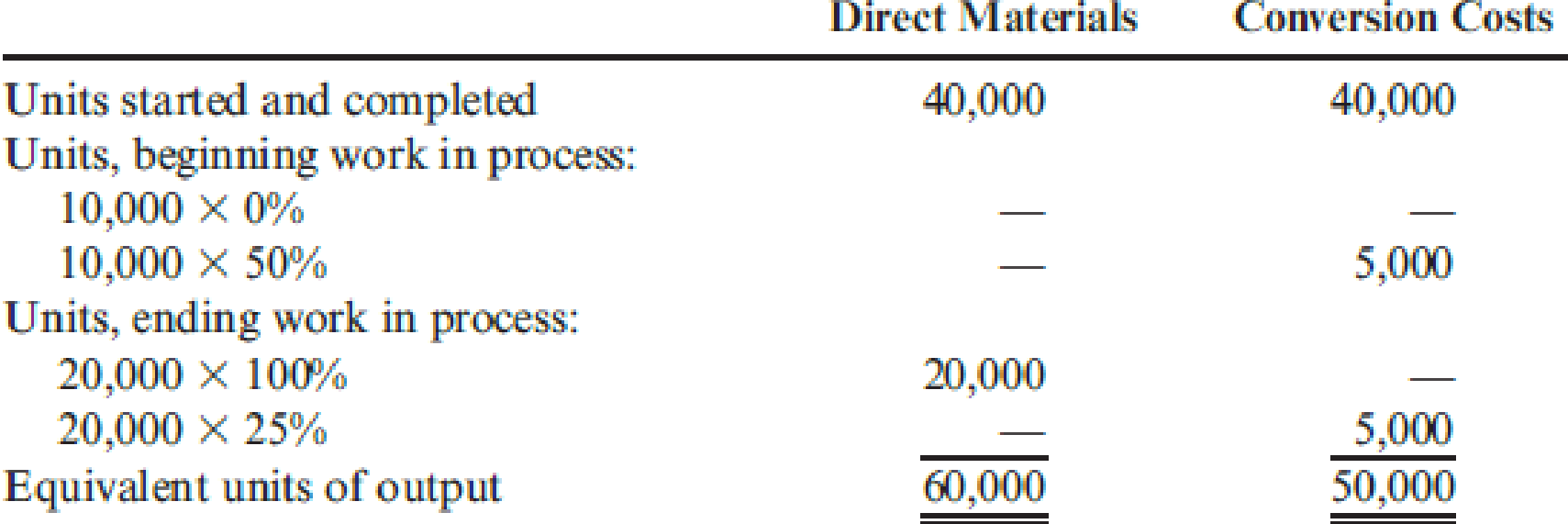

Dama Company produces women’s blouses and uses the FIFO method to account for its

Costs in beginning work in process were direct materials, $20,000; conversion costs, $80,000. Manufacturing costs incurred during April were direct materials, $240,000; conversion costs, $320,000.

Required:

- 1. Prepare a physical flow schedule for April.

- 2. Compute the cost per equivalent unit for April.

- 3. Determine the cost of ending work in process and the cost of goods transferred out.

- 4. Prepare the

journal entry that transfers the costs from Cutting to Sewing.

1.

Prepare the schedule of physical flow.

Explanation of Solution

Process Costing: It is a method of cost accounting used by an enterprise with processes categorised by continuous production. The cost for manufacturing those products are assigned to the manufacturing department before the averaged over units are being produced.

Prepare the schedule of physical flow.

| Particulars | Units |

| Units to account for: | |

| Units, beginning work in process | 10,000 |

| Units started | 60,000 |

| Total units to account for | 70,000 |

| Units accounted for: | |

| Units started completed | 40,000 |

| Units, beginning work in process | 10,000 |

| Units, ending work in process | 20,000 |

| Total units accounted for | 70,000 |

(Table 1)

2.

Calculate the cost per equivalent unit for the month April.

Explanation of Solution

Calculate the cost per equivalent unit for the month April.

Working note 1: Calculate the unit material cost.

Working note 2: Calculate the unit conversion cost.

3.

Ascertain the value of cost of EWIP and the cost of goods transferred out.

Explanation of Solution

Ascertain the value of cost of EWIPs.

| Particulars | Amount in $ |

| Ending work in process: | |

| Direct materials (3) | 80,000 |

| Conversion cost (4) | 32,000 |

| Total cost of ending work in process | 112,000 |

(Table 2)

Ascertain the cost of goods transferred out.

| Particulars | Amount in $ |

| Cost of goods transferred out: | |

| Units started and completed (5) | 416,000 |

| Units, beginning work in process: | |

| Prior-period cost | 100,000 |

| Current costs to finish (6) | 32,000 |

| Total cost of goods transferred out | 548,000 |

(Table 3)

Working note 3: Calculate the units of direct materials during ending work in process.

Working note 4: Calculate the units of conversion cost during ending work in process.

Working note 5: Calculate the value of the units that were started and completed.

Working note 6: Calculate the current cost to finish.

4.

Journalize the given transaction.

Explanation of Solution

Journalize the given transaction.

| Date | Accounts title and explanation |

Debit ($) |

Credit ($) |

| Work in process (Sewing) | 548,000 | ||

| Work in process (Cutting) | 548,000 | ||

| (To record transfer of cost from cutting to sewing) |

(Table 4)

- Work in (sewing) is an asset and there is an increase in the value of an asset. Hence, debit the work in process account by $548,000.

- Work in process (cutting) is an asset and there is a decrease in the value of an asset. Hence, credit the work in process account by $548,000.

Want to see more full solutions like this?

Chapter 6 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Holmes Products, Inc., produces plastic cases used for video cameras. The product passes through three departments. For April, the following equivalent units schedule was prepared for the first department: Costs assigned to beginning work in process: direct materials, 90,000; conversion costs, 33,750. Manufacturing costs incurred during April: direct materials, 75,000; conversion costs, 220,000. Holmes uses the weighted average method. Required: 1. Compute the unit cost for April. 2. Determine the cost of ending work in process and the cost of goods transferred out.arrow_forwardPetrini Products Co. has two departments: Mixing and Cooking. At the beginning of the month, Cooking had 4,000 units in process with costs of 8,600 from Mixing, and its own departmental costs of 500 for materials, 1,000 for labor, and 2,500 for factory overhead. During the month, 10,000 units were received from Mixing with a cost of 25,000. Cooking incurred costs of 4,250 for materials, 8,500 for labor, and 21,250 for factory overhead, and finished 12,000 units. At the end of the month, there were 2,000 units in process, one-half completed. Required: 1. Determine the unit cost for the month in Cooking. 2. Determine the adjusted weighted average unit cost for all units received from Mixing. 3. Determine the unit cost of goods finished. 4. Determine the accumulated cost of the goods finished and of the ending work in process. (Round unit costs to three decimal places.)arrow_forwardBox Springs. Inc., makes two sizes of box springs: queen and king. The direct material for the queen is $35 per unit and $55 is used in direct labor, while the direct material for the king is $55 per unit, and the labor cost is $70 per unit. Box Springs estimates it will make 4,300 queens and 3,000 kings in the next year. It estimates the overhead for each cost pool and cost driver activities as follows: How much does each unit cost to manufacture?arrow_forward

- Haversham Corporation produces dress shirts. The company uses a standard costing system and has set the following standards for direct materials and direct labor (for one shirt): During the year, Haversham produced 9,800 shirts. The actual fabric purchased was 14,600 yards at 2.74 per yard. There were no beginning or ending inventories of fabric. Actual direct labor was 10,900 hours at 19.60 per hour. Required: 1. Compute the costs of fabric and direct labor that should have been incurred for the production of 9,800 shirts. 2. Compute the total budget variances for direct materials and direct labor. 3. Break down the total budget variance for direct materials into a price variance and a usage variance. Prepare the journal entries associated with these variances. 4. Break down the total budget variance for direct labor into a rate variance and an efficiency variance. Prepare the journal entries associated with these variances.arrow_forwardCardiff Inc. manufactures men’s sport shirts for large stores. It produces a single quality shirt in lots of a dozen according to each customer’s order and attaches the store’s label. The standard costs for a dozen shirts include the following: During October, Cardiff worked on three orders for shirts. Job cost records for the month disclose the following: The following information is also available: Cardiff purchased 95,000 yards of materials during October at a cost of $53,200. The materials price variance is recorded when goods are purchased, and all inventories are carried at standard cost. Direct labor incurred amounted to $112,750 during October. According to payroll records, production employees were paid $10.25 per hour. Overhead is applied on the basis of direct labor hours. Factory overhead totaling $22,800 was incurred during October. A total of $288,000 was budgeted for overhead for the year, based on estimated production at the plant’s normal capacity of 48,000 dozen shirts per year. Overhead is 60% fixed and 40% variable at this level of production. There was no work in process at October 1. During October, Lots 30 and 31 were completed, and all materials were issued for Lot 32, which was 80% completed as to labor and overhead. Required: Prepare a schedule computing the October total standard cost of Lots 30, 31, and 32. Prepare a schedule computing the materials price variance for October and indicate whether it is favorable or unfavorable. For each lot produced during October, prepare schedules computing the following (indicate whether favorable or unfavorable): Materials quantity variance in yards. Labor efficiency variance in hours. (Hint: Don’t forget the percentage of completion.) Labor rate variance in dollars. Prepare a schedule computing the total flexible-budget and production-volume overhead variances for October and indicate whether they are favorable or unfavorable. Give some reasons as to why the production-volume variance may be unfavorable and why it is important to correct the situation.arrow_forwardJacson Company produces two brands of a popular pain medication: regular strength and extra strength. Regular strength is produced in tablet form, and extra strength is produced in capsule form. All direct materials needed for each batch are requisitioned at the start. The work orders for two batches of the products are shown below, along with some associated cost information: In the Mixing Department, conversion costs are applied on the basis of direct labor hours. Budgeted conversion costs for the department for the year were 60,000 for direct labor and 190,000 for overhead. Budgeted direct labor hours were 5,000. It takes one minute of labor time to mix the ingredients needed for a 100-unit bottle (for either product). In the Bottling Department, conversion costs are applied on the basis of machine hours. Budgeted conversion costs for the department for the year were 400,000. Budgeted machine hours were 20,000. It takes one-half minute of machine time to fill a bottle of 100 units. Required: 1. What are the conversion costs applied in the Mixing Department for each batch? The Bottling Department? 2. Calculate the cost per bottle for the regular and extra strength pain medications. 3. Prepare the journal entries that record the costs of the 12,000 regular strength batch as it moves through the various operations. 4. Suppose that the direct materials are requisitioned by each department as needed for a batch. For the 12,000 regular strength batch, direct materials are requisitioned for the Mixing and Bottling departments. Assume that the amount of cost is split evenly between the two departments. How will this change the journal entries made in Requirement 3?arrow_forward

- Foamy Inc. manufactures shaving cream and uses the weighted average cost method. In November, production is 14,800 equivalent units for materials and 13,300 units for labor and overhead. During the month, materials, labor, and overhead costs were as follows: Beginning work in process for November had a cost of 11,360 for materials, 11,666 for labor, and 9,250 for overhead. Compute the following: a. Weighted average cost per unit for materials b. Weighted average cost per unit for labor c. Weighted average cost per unit for overhead d. Total unit cost for the montharrow_forwardKenkel, Ltd. uses backflush costing to account for its manufacturing costs. The trigger points are the purchase of materials, the completion of goods, and the sale of goods. Prepare journal entries to account for the following: a. Purchased raw materials, on account, 80,000. b. Requisitioned raw materials to production, 80,000. c. Distributed direct labor costs, 10,000. d. Factory overhead costs incurred, 60,000. (Use Various Credits for the account in the credit part of the entry.) e. Completed all of the production started. f. Sold the completed production for 225,000, on account.arrow_forwardFrenchys makes two types of scarves: polyester (poly) and silk. There are two cost pools: setup, with an estimated $120,000 in overhead, and inspection, with $30,000 in overhead. Poly is estimated to have 800,000 setups and 450,000 inspections, while silk has 400,000 setups and 150,000 inspections. How much overhead is applied to each product?arrow_forward

- JoyT Company manufactures Maxi Dolls for sale in toy stores. In planning for this year, JoyT estimated variable factory overhead of 600,000 and fixed factory overhead of 400,000. JoyT uses a standard costing system, and factory overhead is allocated to units produced using standard direct labor hours. The level of activity budgeted for this year was 10,000 direct labor hours, and JoyT used 10,300 actual direct labor hours. Based on the output accomplished during this year, 9,900 standard direct labor hours should have been used. Actual variable factory overhead was 596,000, and actual fixed factory overhead was 410,000 for the year. Based on this information, the variable factory overhead controllable variance for JoyT for this year was: a. 24,000 unfavorable. b. 2,000 unfavorable. c. 4,000 favorable. d. 22,000 favorable.arrow_forwardBox Springs, Inc., makes two sizes of box springs: twin and double. The direct material for the twin is $25 per unit and $40 s used in direct labor, while the direct material for the double is $40 per unit, and the labor cost is $50 per unit. Box Springs estimates it will make 5,000 twins and 9,000 doubles in the next year. It estimates the overhead for each cost pool and cost driver activities as follows: How much does each unit cost to manufacture?arrow_forwardNarwhal Swimwear has a beginning work in process inventory of 13,500 units and transferred in 130,000 units before ending the month with 14,000 units that were 100% complete with regard to materials and 30% complete with regard to conversion costs. The cost per unit of material is $5.80 and the cost per unit for conversion is $8.20 per unit. Using the weighted-average method, what is the amount of material and conversion costs assigned to the department for the month?arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,