Videos

A firm experienced the

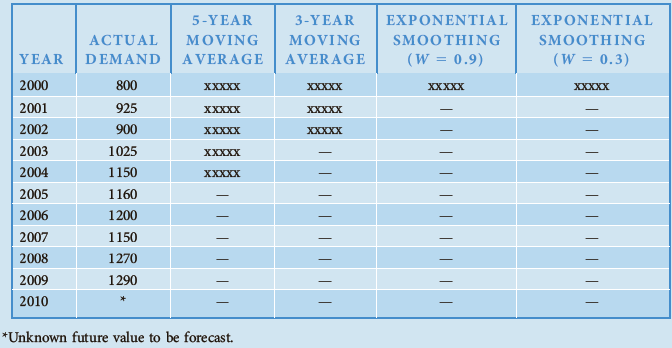

*Unkown future value to be forecast

- Fill in the table by preparing forecasts based on a five-year moving average, a three-year moving average, and exponential smoothing (with a

-

- Using the forecasts from 2005 through 2009, compare the accuracy of each of the

forecasting methods based on the RMSE criterion. - Which forecast would you have used for 2010? Why?

a)

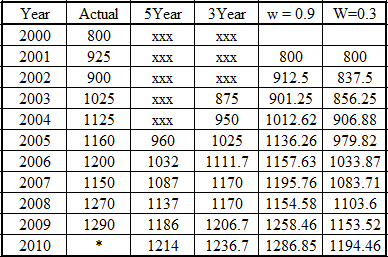

To complete: The missing values in the table.

Explanation of Solution

To fill 5th year column. Use below formula.

Similarly, for 3year column.

For exponential smoothing:

Let the value forecasted value for 2000 is zero and assume the forecast value of 2001 is 800.

b)

To compare: The accuracy of forecast methods.

Explanation of Solution

Root mean square error is used to find the accuracy.

| Year | Actual value (Yt) | Forecast ( | ||

| 2005 | 1160 | 960 | 200 | 40000 |

| 2006 | 1200 | 1032 | 168 | 28224 |

| 2007 | 1150 | 1087 | 63 | 3969 |

| 2008 | 1270 | 1137 | 133 | 17689 |

| 2009 | 1290 | 1186 | 104 | 10816 |

Now calculate the RMSE.

Now calculate the RMSE for 3 year moving average.

| Year | Actual value (Yt) | Forecast ( | ||

| 2005 | 1160 | 1025 | 135 | 18225 |

| 2006 | 1200 | 1112 | 88 | 7744 |

| 2007 | 1150 | 1170 | -20 | 400 |

| 2008 | 1270 | 1170 | 100 | 10000 |

| 2009 | 1290 | 1207 | 83 | 6889 |

Calculate RMSE.

Now calculate the RMSE when w = 0.9

| Year | Actual value (Yt) | Forecast ( | ||

| 2005 | 1160 | 1136.26 | 23.74 | 563.5876 |

| 2006 | 1200 | 1157.63 | 42.37 | 1795.217 |

| 2007 | 1150 | 1195.76 | -45.76 | 2093.978 |

| 2008 | 1270 | 1154.58 | 115.42 | 13321.78 |

| 2009 | 1290 | 1258.46 | 31.54 | 994.7716 |

Now calculate the RMSE when w = 0.3

| Year | Actual value (Yt) | Forecast ( | ||

| 2005 | 1160 | 979.82 | 180.18 | 32464.83 |

| 2006 | 1200 | 1033.87 | 166.13 | 27599.18 |

| 2007 | 1150 | 1083.71 | 66.29 | 4394.364 |

| 2008 | 1270 | 1103.71 | 166.4 | 27688.96 |

| 2009 | 1290 | 1153.52 | 136.48 | 18626.79 |

Conclusion: The lowest value of RMSE reflects the greater accuracy. Therefore, when w = 0.9 then RMSE shows most accurate model.

c)

To Find: The method used to forecast.

Explanation of Solution

Since the greater accuracy come for the exponential smoothening with w = 0.9. Thus, same will be used to forecast the demand of 2010.

Want to see more full solutions like this?

Chapter 5 Solutions

Managerial Economics: Applications, Strategies and Tactics (MindTap Course List)

- Plot the logarithm of arrivals for each transportation mode against time, all on the same graph. Which now appears to be growing the fastest?arrow_forwardSavings-Mart (a chain of discount department stores) sells patio and lawn furniture. Sales are seasonal, with higher sales during the spring and summer quarters and lower sales during the fall and winter quarters. The company developed the following quarterly sales forecasting model: Y t=8.25+0.125t2.75D1t+3.50D3t where Y t=predictedsales(million)inquartert 8.25=quarterlysales(million)whent=0 t=timeperiod(quarter)wherethefourthquarterof2002=0,firstquarterof2003=1,secondquarterof2003=2,... D1t={1forfirst-quarterobservations0otherwiseD2t={1forsecond-quarterobservations0otherwiseD3t={1forthird-quarterobservations0otherwise Forecast Savings-Marts sales of patio and lawn furniture for each quarter of 2010.arrow_forwardThe forecasting staff for the Prizer Corporation has developed a model to predict sales of its air-cushioned-ride snowmobiles. The model specifies that sales S vary jointly with disposable personal income Y and the population between ages 15 and 40, Z, and inversely with the price of the snowmobiles P. Based on past data, the best estimate of this relationship is S=kYZP where k has been estimated (with past data) to equal 100. If Y=11,000,Z=1,200, and P=20,000, what value would you predict for S? What happens if P is reduced to $17,500? How would you go about developing a value for k? What are the potential weaknesses of this model?arrow_forward

- Metropolitan Hospital has estimated its average monthly bed needs as N=1,000+9X where X=timeperiod(months);January2002=0 N=monthlybedneeds Assume that no new hospital additions are expected in the area in the foreseeable future. The following monthly seasonal adjustment factors have been estimated, using data from the past five years: Forecast Metropolitans bed demand for January, April, July, November, and December 2007. If the following actual and forecast values for June bed demands have been recorded, what seasonal adjustment factor would you recommend be used in making future June forecasts?arrow_forwardHistorical demand for Peeps is as displayed in the table. Month Demand January 11 February 18 March 31 April 39 May 44 June 53 July 67 August 82 September 96 Develop forecasts from June through October using these techniques: Holt's method with alpha=0.2 and beta=0.1. For Holt's model, the level and trend for May are assumed to be 44 and 12. Judge which forecast method is the best based on MAD.arrow_forward4. Suppose we have a summary of forecasting techniques calculation results for Gundam Auto Sales Inc. (in the prior item) as follows: Mean Next Standard Period Error Forecasting Method Used Forecast (MSE) 1.3-period UnWMA 10.42 3.24 2.4-period UnWMA 10.38 3.51 3.3-period WMA 10.83 3.03 4. Simple Exponential Smoothing 5. Trend Projection 8.24 5.04 11.43 1.16 a. Which among the techniques is the most reliable? b. What does the result of the most reliable technique say?arrow_forward

- Director Very Busy needs to allocate time this week for office appointments, so he needs to forecast the number of employees who will seek appointments. The director has gathered the following time series data recently Period Employee Appointments 4 weeks ago 95 3 weeks ago 80 2 week ago 65 last week 50arrow_forwardEconomics You own a restaurant near the beach. Business has been growing each year, but obviously spikes during the summer months. A regression produces the following equation: M = 30,000 + 500t + 1,000S Where M is monthly sales, t is years past 2010, and S is a dummy variable for the summer months. If the month is June, July, or August, insert a "1". If not, the value for S is zero. What are the predicted sales for July 2020? Enter as a value.arrow_forwardMr. Geppetto uses exponential smoothing to predict revenue in his wood carving business. He uses a weight of = .4 for the naïve forecast and (1-) = .6 for the past forecast. What revenue did he predict for March using the data below? MONTH REVENUE FORECAST Nov 100 100 Dec 90 100 Jan 115 ---- Feb 110 ---- MARCH ? ?arrow_forward

- The Carbondale Hospital is considering the purchase of a new ambulance. The decision will rest partly on the anticipated mileage to be driven next year. The miles driven during the past 5 years are as follows: Year Mileage 1 3,050 a) Using a 2-year moving average, the forecast for year 6 = miles (round your response to the nearest whole number). b) If a 2-year moving average is used to make the forecast, the MAD based on this = miles (round your response to one decimal place). (Hint: You will have only 3 years of matched data.) c) The forecast for year 6 using a weighted 2-year moving average with weights of 0.45 and 0.55 (the weight of 0.55 is for the most recent period) = miles (round your response to the nearest whole number). The MAD for the forecast developed using a weighted 2-year moving average with weights of 0.45 and 0.55 = d) Using exponential smoothing with a = 0.20 and the forecast for year 1 being 3,050, the forecast for year 6 = miles (round your response to one decimal…arrow_forwardOA linear regression model is Units 3,414-0.839xWeek. For week 45, what is the forecast for the number of units? Round your answer to the nearest whole number. OO unitsarrow_forwardYou own a restaurant near the beach. Business has been growing each year, but obviously spikes during the summer months. A regression produces the following equation: M = 30,000 + 500t + 1,000S Where M is monthly sales, t is years past 2010, and S is a dummy variable for the summer months. If the month is June, July, or August, insert a "1"”. If not, the value for S is zero. What are the predicted sales for July 2020? Enter as a value.arrow_forward

Managerial Economics: Applications, Strategies an...EconomicsISBN:9781305506381Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. HarrisPublisher:Cengage Learning

Managerial Economics: Applications, Strategies an...EconomicsISBN:9781305506381Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. HarrisPublisher:Cengage Learning