Concept Introduction

Marginal Cost: This refers to the change in the cost which is incurred when an additional unit of any good or service is produced. It shall be calculated as follows:

Shut-down Price: This is the level of price when the revenue is equal to the variable cost. This happens when the price is equal to the lowest

Explanation of Solution

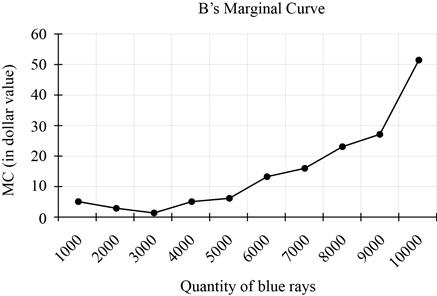

a. Graph to show Bob’s marginal cost curve.

The below table shows the calculation of marginal cost:

| Quantity Produced(A) | Change in Quantity(B) | Fixed Cost($)(C) | Variable Cost($)(D) | Total Cost($)(E) | Change in Total Cost($)(F) | Marginal Cost($) |

| 0 | - | 50,000 | 0 | 50,000 | - | - |

| 1,000 | 1,000 | 50,000 | 5,000 | 55,000 | 5,000 | 5 |

| 2,000 | 1,000 | 50,000 | 8,000 | 58,000 | 3,000 | 3 |

| 3,000 | 1,000 | 50,000 | 9,000 | 59,000 | 1,000 | 1 |

| 4,000 | 1,000 | 50,000 | 14,000 | 64,000 | 5,000 | 5 |

| 5,000 | 1,000 | 50,000 | 20,000 | 70,000 | 6,000 | 6 |

| 6,000 | 1,000 | 50,000 | 33,000 | 83,000 | 13,000 | 13 |

| 7,000 | 1,000 | 50,000 | 49,000 | 99,000 | 16,000 | 16 |

| 8,000 | 1,000 | 50,000 | 72,000 | 122,000 | 23,000 | 23 |

| 9,000 | 1,000 | 50,000 | 99,000 | 149,000 | 27,000 | 27 |

| 10,000 | 1,000 | 50,000 | 150,000 | 200,000 | 51,000 | 51 |

As per the marginal cost calculated in the above table, below is the graph that shows Bob’s marginal cost curve:

Fig 1

Conclusion:

Thus, the above graph shows the marginal curve drawn from the marginal costs calculated.

b. Range of price over which Mr. Bob will produce no units.

The below table shows the calculation of average variable cost:

| Quantity Produced(A) | Variable Cost($)(B) | Average Variable Cost($) |

| 0 | 0 | 0 |

| 1,000 | 5,000 | 5 |

| 2,000 | 8,000 | 4 |

| 3,000 | 9,000 | 3 |

| 4,000 | 14,000 | 3.5 |

| 5,000 | 20,000 | 4 |

| 6,000 | 33,000 | 5.5 |

| 7,000 | 49,000 | 7 |

| 8,000 | 72,000 | 7 |

| 9,000 | 99,000 | 11 |

| 10,000 | 150,000 | 15 |

Shut-down price is the level when the price is equal to the lowest average variable cost. Thus, as per the above table, the shut-down price is $3.

Mr. Bob will not produce any quantity when the price of a product falls below the shut-down price, which is $3. Hence, the range of price over which there will be no production is $0 to $3.

Conclusion:

Thus, the range of prices where there will be no production is $0 to $3.

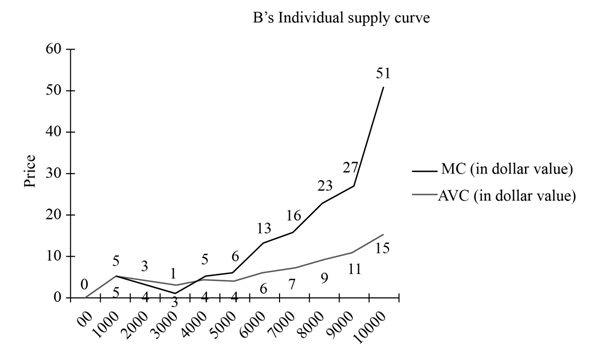

c. Graph to show Mr. Bob’s individual supply curve.

The below table shows the marginal cost and average variable cost of Mr. Bob:

| Quantity Produced | Marginal Cost($) | Average Variable Cost($) |

| 0 | - | 0 |

| 1,000 | 5 | 5 |

| 2,000 | 3 | 4 |

| 3,000 | 1 | 3 |

| 4,000 | 5 | 3.5 |

| 5,000 | 6 | 4 |

| 6,000 | 13 | 5.5 |

| 7,000 | 16 | 7 |

| 8,000 | 23 | 7 |

| 9,000 | 27 | 11 |

| 10,000 | 51 | 15 |

As per the marginal cost and average variable cost in the above table, below is the graph that shows Bob’s individual supply curve:

Fig 2

- The above graph shows that Mr. Bob will continue the production only if the price is above $3 which is the shut-down price.

- Hence, the production level at prices below the shut-down price of $3 is nil.

Conclusion:

Thus, the graph is shown for Mr. Bob’s individual supply curve.

Want to see more full solutions like this?

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education