Videos

Enterprise Fund

Required

- a. For fiscal year 2020, prepare general journal entries for the Water Utility Fund using the following information.

- 1. The amount in the Accrued Utility Revenue account was reversed.

- 2. Billings to customers for water usage during fiscal year 2020 totaled $2,982,557; $193,866 of the total was billed to the General Fund.

- 3. Cash in the amount of $260,000 was received. The cash was for interest earned on investments and $82,000 in accrued interest.

- 4. Expenses accrued for the period were management and administration, $360,408; maintenance and distribution, $689,103; and treatment plant, $695,237.

- 5. Cash receipts for customer deposits totaled $2,427.

- 6. Cash collections on customer accounts totaled $2,943,401, of which $209,531 was from the General Fund.

- 7. Cash payments for the period were as follows: Accounts Payable, $1,462,596; interest (which includes the interest payable), $395,917; bond principal, $400,000; machinery and equipment, $583,425; and return of customer deposits, $912.

- 8. A state grant amounting to $475,000 was received to help pay for new water treatment equipment.

- 9. Accounts written off as uncollectible totaled $10,013.

- 10. The utility fund transferred $800,000 in excess operating income to the General Fund.

- 11.

Adjusting entries for the period were recorded as follows:depreciation on buildings was $240,053 and on machinery and equipment was $360,079; the allowance for uncollectible accounts was increased by $14,913; an accrual for unbilled customer receivables was made for $700,000; accrued interest income was $15,849; and accrued interest expense was $61,406. - 12. The Revenue Bond Payable account was adjusted by $400,000 to record the current portion of the bond.

- 13. Closing entries and necessary adjustments were made to the net position accounts.

- b. Prepare a statement of revenues, expenses, and changes in fund net position for the Water Utility Fund for the year ended June 30, 2020.

- c. Prepare a statement of net position for the Water Utility Fund as of June 30, 2020.

- d. Prepare a statement of

cash flows for the Water Utility Fund as of June 30, 2020.

a.

Prepare journal entries to record the transactions of Water Utility Fund.

Explanation of Solution

Enterprise funds: The enterprise funds record the activities that provide goods or service to the public. The enterprise funds are treated similar to that of business organizations.

Journal: Journal is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Rules of Debit and Credit: Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

Prepare journal entry to reverse the “accrued utility revenue account”:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Sales of water | 500,000 | |||

| Accrued utility revenues | 500,000 | |||

| (To record the reverse of accrued utility revenue account) |

Table (1)

Prepare journal entry to record the accrual of revenue from the sale of water:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Accounts Receivable | 2,788,691 | |||

| Due from General fund | 193,866 | |||

| Sales of water | 2,982,557 | |||

| (To record the accrual of revenue from the sale of water) |

Table (2)

Prepare journal entry to record the interest income received and accrued:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Cash | 260,000 | |||

| Interest Income | 178,000 | |||

| Interest Receivable | 82,000 | |||

| (To record the interest income received and accrued) |

Table (3)

Prepare journal entry to record the accrual of expenses:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Management and administrative expense | 360,408 | |||

| Maintenance and Distribution | 689,103 | |||

| Treatment Plant Expense | 695,237 | |||

| Accounts Payable | 1,744,748 | |||

| (To record the accrual of expenses) |

Table (4)

Prepare journal entry to record the cash receipt for customer deposits:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Cash (restricted) | 2,427 | |||

| Customer deposits | 2,427 | |||

| (To record the cash receipts for customer deposits) |

Table (5)

Prepare journal entry to record the cash collected on customer account and general fund:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Cash | 2,943,401 | |||

| Accounts Receivable | 2,733,870 | |||

| Due from General Fund | 209,531 | |||

| (To record the cash collected on customer account and general fund) |

Table (6)

Prepare journal entry to record the payment of expenses and return of customer deposit:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Accounts Payable | 1,462,596 | |||

| Interest expense | 264,145 | |||

| Interest Payable | 131,772 | |||

| Current portion of long-term debt | 400,000 | |||

| Machinery and equipment | 583,425 | |||

| Customer deposits | 912 | |||

| Cash ($2,943,401-$209,531) | 2,841,938 | |||

| Cash (restricted) | 912 | |||

| (To record the payment of expenses and return of customer deposits) |

Table (7)

Prepare journal entry to record the receipt of state grant:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Cash | 475,000 | |||

| Contribution(capital grant) | 475,000 | |||

| (To record the receipt of grant from the state) |

Table (8)

Prepare journal entry to write off the uncollectible accounts:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Allowance for uncollectible account | 10,013 | |||

| Accounts receivable | 10,013 | |||

| (To record the write off the uncollectible account) |

Table (9)

Prepare the journal entry to record the inter-fund fund transfer:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Interfund transfer- General fund | 800,000 | |||

| Cash | 800,000 | |||

| (To record the receipt of funds from general fund) |

Table (10)

Prepare journal entry to record the depreciation expense on building:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Depreciation expense - Building | 240,053 | |||

| Allowance for depreciation - Building | 240,053 | |||

| (To record the depreciation expense on building) |

Table (11)

Prepare journal entry to record the depreciation expense on machinery and equipment:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Depreciation expense – Machinery and equipment | 360,079 | |||

| Allowance for depreciation - Machinery and equipment | 360,079 | |||

| (To record the depreciation expense on machinery and equipment) |

Table (12)

Prepare journal entry to create provision for uncollectible accounts:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Provision for uncollectible account | 14,913 | |||

| Allowance for uncollectible account | 14,913 | |||

| (To record the increase in uncollectible account) |

Table (13)

Prepare journal entry to record the accrual of utility revenues:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Accrued Utility Revenue | 700,000 | |||

| Sales of Water | 700,000 | |||

| (To record the increase in uncollectible account) |

Table (14)

Prepare journal entry to record the accrual of interest income:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Interest Receivable | 15,849 | |||

| Interest Income | 15,849 | |||

| (To record the accrual of interest income) |

Table (15)

Prepare journal entry to record the accrual of interest expense:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Interest Expense | 61,406 | |||

| Interest Payable | 61,406 | |||

| (To record the accrual of interest expense) |

Table (16)

Prepare journal entry to adjust the revenue bond payable and record the current portion of long-term debt:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Revenue bonds payable | 400,000 | |||

| Current portion of long-term debt | 400,000 | |||

| (To record the current portion of long-term debt) |

Table (17)

Prepare journal entry to close all the nominal accounts:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Sales of water | 3,182,557 | |||

| Interest income | 193,849 | |||

| Contribution (capital grant) | 475,000 | |||

| Management and administrative expense | 360,408 | |||

| Maintenance and distribution | 689,103 | |||

| Treatment plant expense | 695,237 | |||

| Interfund transfer- general fund | 800,000 | |||

| Interest Expense | 325,551 | |||

| Depreciation expense-building | 240,053 | |||

| Depreciation expense- machinery and equipment | 360,079 | |||

| Uncollectible account | 14,913 | |||

| Net position-unrestricted (balancing figure) | 366,062 | |||

| (To record closing of nominal accounts) |

Table (18)

Prepare journal entry to allocate the increase in “net investment in capital assets” to the “unrestricted net position”:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| Net position -Unrestricted | 383,293 | |||

| Net position-net investment in capital assets | 383,293 | |||

| (To record the increase in “net investment in capital assets” to the “unrestricted net position) |

Table (19)

Working note: Determine the amount of increase in the “net investments in capital assets”.

Step 1: Calculate the ending balance of “net investments in capital assets”.

Step 2: Calculate the amount of increase in the “net investments in capital assets”.

b.

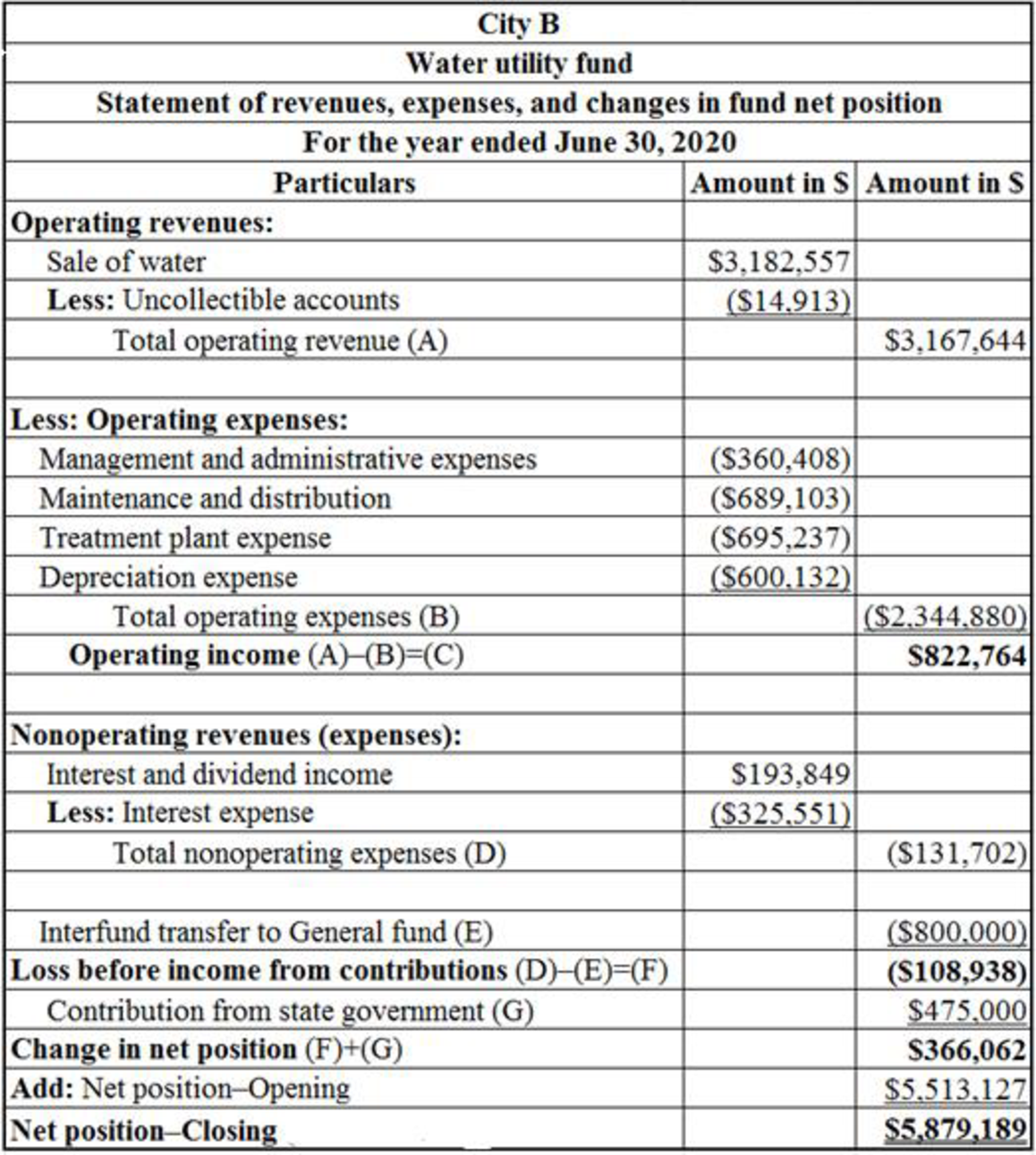

Prepare a “statement of revenues, expenses, and changes in fund net position” for Central Station Fund.

Explanation of Solution

Statement of revenues, expenses and changes in net position: Statement of activities is the operating statement that reports revenues, expenses, and changes in net position during the year.

Prepare a “statement of revenues, expenses, and changes in fund net position” for Water utility fund.

Table (20)

Working note: Determine the amount of net position-opening.

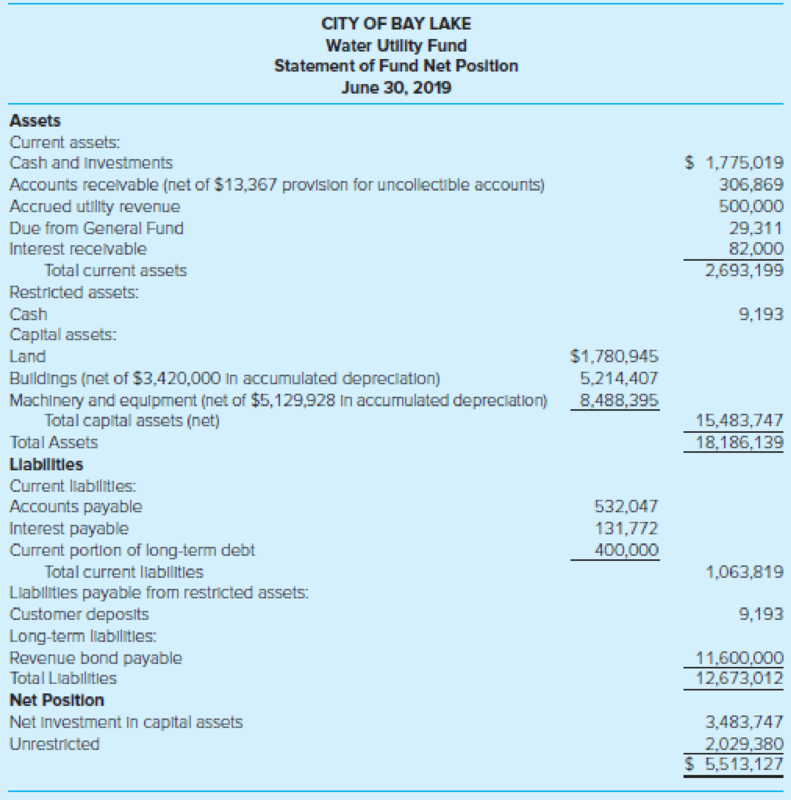

Before the fiscal year adjustment, the amount of unrestricted net position is $2,029,380 and the net position of “net investment is capital assets” calculated above is $3,483,747. Hence, the total net position-Opening is $5,513,127

(c)

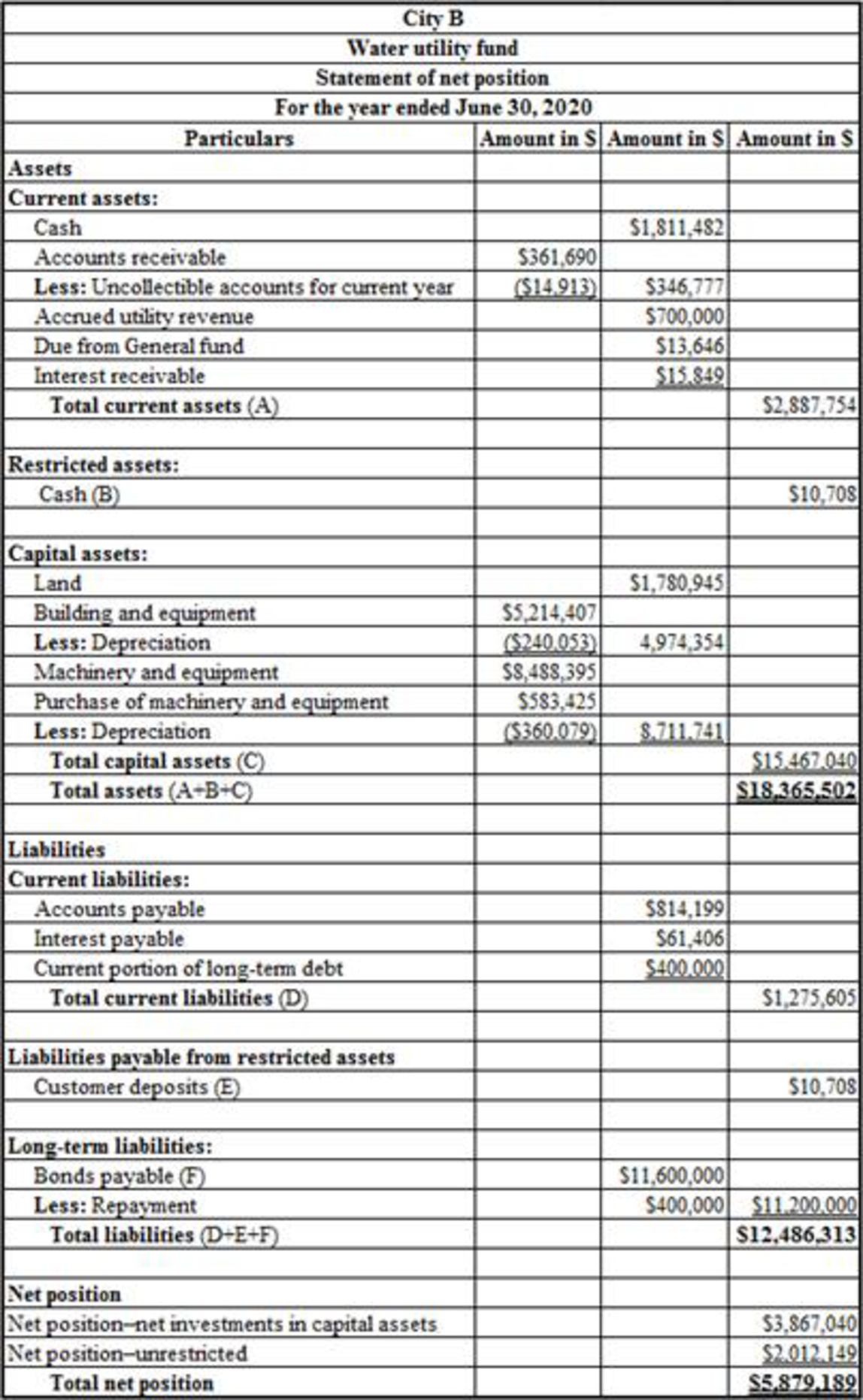

Prepare a “statement of net position” for Water Utility Fund.

Explanation of Solution

Statement of net position: Statement of financial position is a balance sheet that reports the assets, deferred outflow of resources, liabilities, deferred inflow of resources and the residual amount or net position of the government at the end of the fiscal year.

Prepare a “statement of net position” for Water Utility Fund.

Table (21)

Working notes:

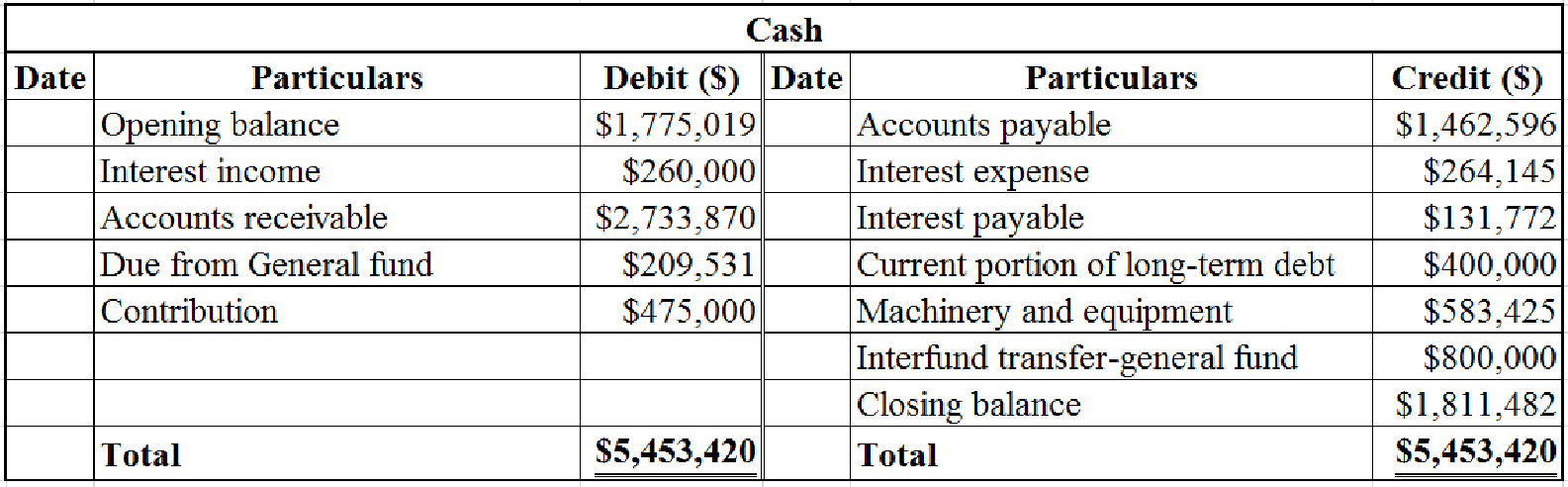

- Determine the closing balance of cash account.

Table (22)

- Determine the closing balance of accounts receivable.

Table (23)

- Determine the closing balance of accrued utility revenue.

Table (24)

- Determine the closing balance of “due from general fund”.

Table (25)

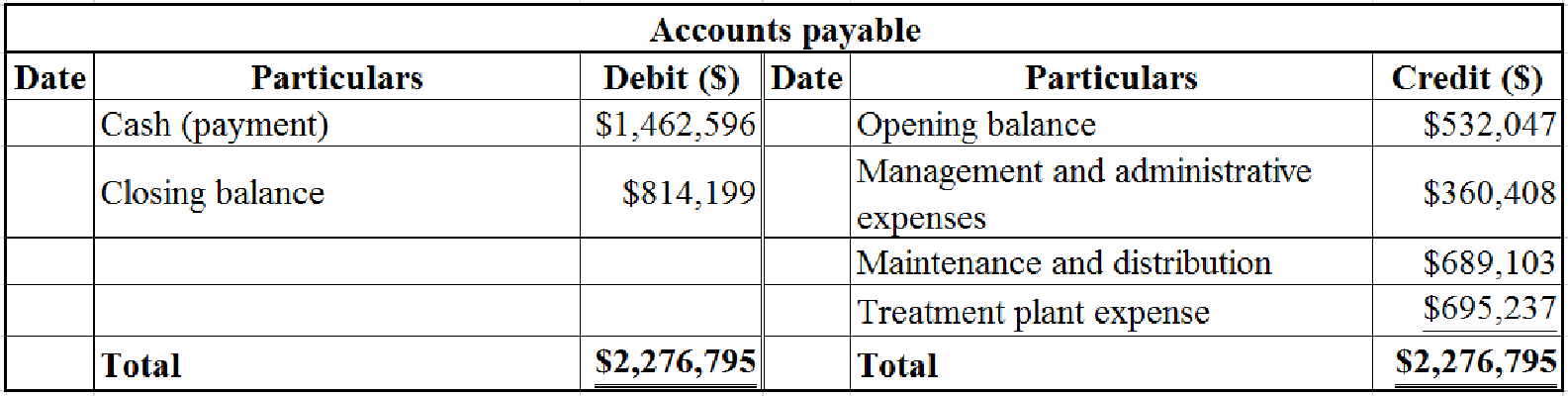

- Determine the closing balance of accounts payable.

Table (26)

- Determine the closing balance of customer deposits.

Table (27)

- Determine the net position of unrestricted assets as on June 30, 2020.

(d)

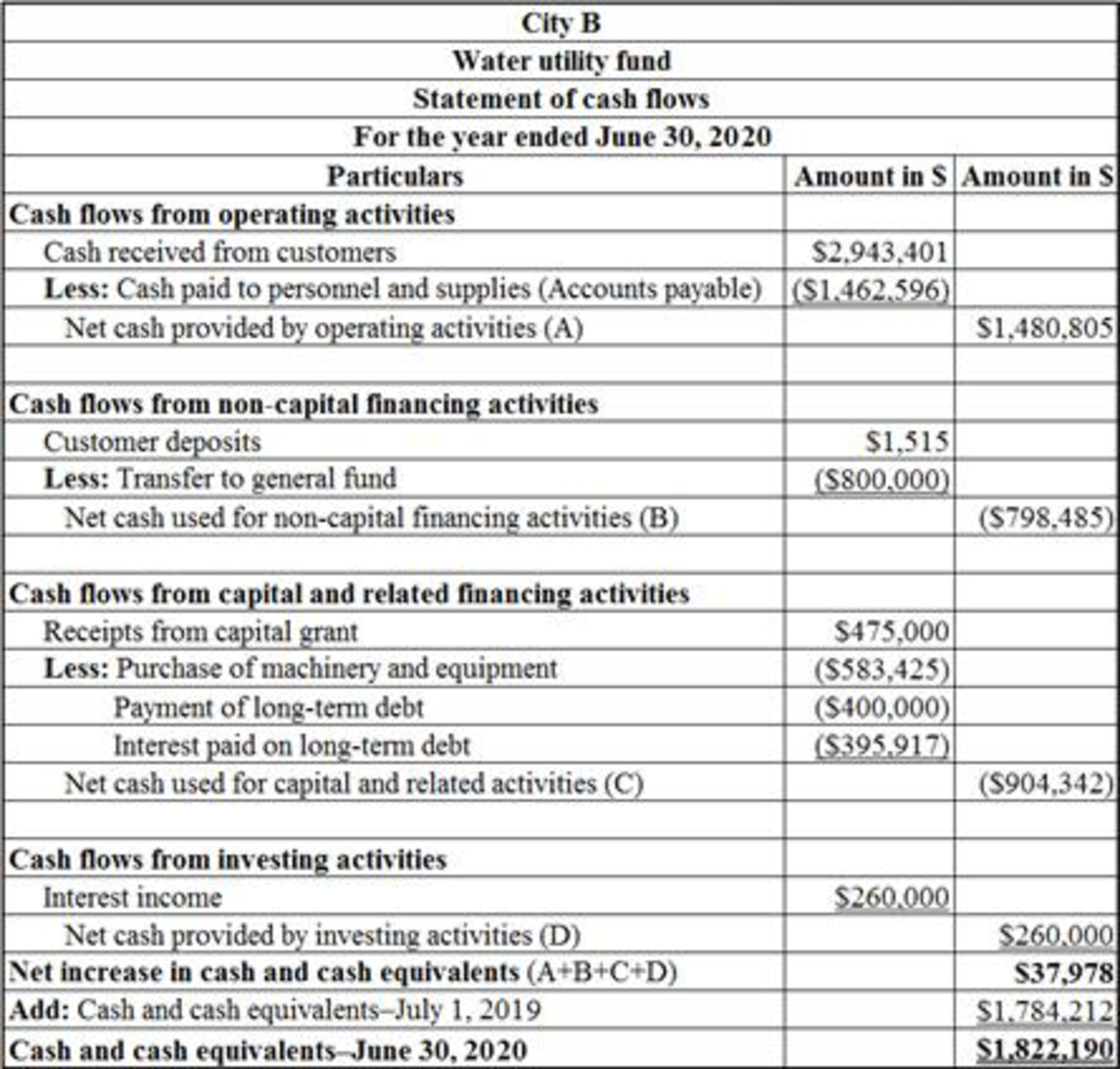

Prepare “a statement of cash flows” for water Utility Fund.

Explanation of Solution

Statement of cash flows: Statement of cash flow is a financial statement that shows the cash and cash equivalents of a company for a particular period of time. It shows the net changes in cash, by reporting the sources and uses of cash as a result of operating, investing, and financing activities of a company.

Prepare “a statement of cash flows” for water Utility Fund.

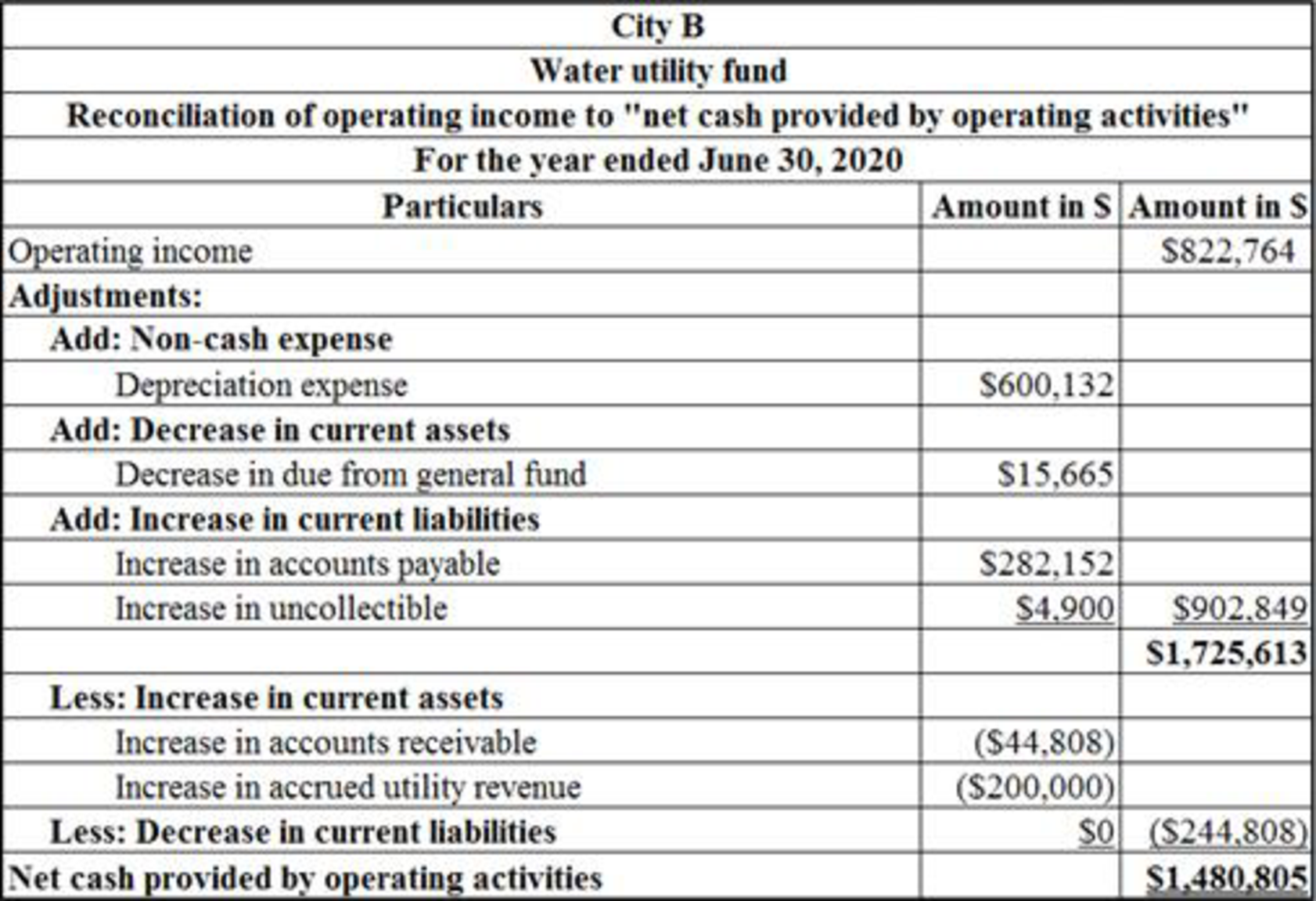

Step 1: Prepare the reconciliation statement to reconcile the operating loss with the “net cash used for operating activities”.

Table (28)

Working notes:

- Determine the increase in accounts payable.

The opening balance of accounts payable is $532,047 and the closing balance of accounts payable is $814,199. Hence, the accounts payable is increased by $282,152

- Determine the increase in “due from general fund”.

The opening balance of “due from general fund” is $29,311 and the closing balance of “due from general fund” is $13,646. Hence, the “due from general fund” is decreased by $15,665

- Determine the balance in provision for uncollectible account.

Table (29)

- Determine the increase in uncollectible.

The opening balance of uncollectible is $13,367 and the closing balance of uncollectible is $18,267. Hence, the uncollectible is increased by $4,900

- Determine the increase in accounts receivable.

The opening balance of accounts receivable is $306,869. The closing balance of accounts receivable is $361,690. The written off portion of accounts receivable is $10,013. So, the net closing balance of accounts receivable is $351,677

- Determine the increase in accrued utility revenue.

The opening balance of accrued utility revenue is $500,000 and the closing balance of accrued utility revenue is $700,000. Hence, the accrued utility revenue is increased by $200,000

Step 2: Prepare “a statement of cash flows”.

Table (30)

Want to see more full solutions like this?

Chapter 7 Solutions

Accounting For Governmental & Nonprofit Entities

- Required information [The following information applies to the questions displayed below.] The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2024, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund. Accounts payable Accounts receivable Accrued interest payable Accumulated depreciation Administrative and selling expenses Allowance for uncollectible accounts Capital assets Cash Charges for sales and services Cost of sales and services Depreciation expense Due from General Fund Interest expense Interest revenue Transfer in from General Fund Bank note payable Supplies inventory Totals Debits Adjustments: $ 29,400 53,000 VILLAGE OF SEASIDE PINES ENTERPRISE FUND Reconciliation of Operating Income to Net Cash Provided by Operating Activities For the year ended December 31, 2024 722,000 98,000 504,000 51,000 17,700 40,900 19,700 $ 1,535,700 Credits $ 112,000 32,600 51,000…arrow_forwardActivities of a county recreation center are reported in an enterprise fund. During 2019, $5,000,000 is spent on equipment and bonds are issued for $3,000,000. How are these two transactions reported on the enterprise fund’s operating statement? a. No effect b. Revenues, $3,000,000; expenditures, $5,000,000 c. Other financing sources, $3,000,000 d. Other financing sources, $3,000,000; expenditures, $5,000,000arrow_forward4. The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2020, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund. Accounts payable Accounts receivable Accrued interest payable Accumulated depreciation Administrative and selling expenses Allowance for uncollectible accounts Capital assets Cash Charges for sales and services Cost of sales and services Depreciation expense Due from General Fund Interest expense Interest revenue Transfer in from General Fund Bank note payable Supplies inventory Totals Debits $32,000 47,000 712,000 89,000 479,000 45,000 17,000 40,000 18,000 $1,479,000 Credits $ 96,000 28,000 45,000 12,000 550,000 4,000 119,000 625,000 $1,479,000 Required: a. Prepare the closing entries for December 31. b. Prepare the Statement of Revenues, Expenses, and Changes in Fund Net Position for the year ended December 31. c. Prepare the Net Position section of the…arrow_forward

- ! Required information [The following information applies to the questions displayed below.] The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2020, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund. Accounts payable Accounts receivable Accrued interest payable Accumulated depreciation Administrative and selling expenses Allowance for uncollectible accounts Capital assets Cash Charges for sales and services Cost of sales and services Depreciation expense Due from General Fund Debits $ Credits 96,000 $ 32,000 28,000 45,000 47,000 12,000 712,000 89,000 550,000 479,000 45,000 17,000 Interest expense Interest revenue Transfer in from General Fund Bank note payable Supplies inventory Totals 40,000 18,000 4,000 119,000 625,000 $1,479,000 $1,479,000 Prepare the reconciliation of operating income to net cash provided by operating activities that would appear at the bottom of…arrow_forwardFrom the information given above, prepare a General Fund Statement of Revenues, Expenditures, and Changes in Fund Balances for the City of Eastern Shores General Fund for the year ended September 30, 2020. (Negative entries should be entered with a minus sign and will appear in parenthesis.)arrow_forwardCalculate operating margin Assume the following information was derived from the fund financial statements prepared by the city of Tallahassee, Florida for the fiscal year ended September 30, 2019: Assets: City of Tallahassee General Fund Balance Sheet (in thousands) Cash and cash equivalents Due from other governments All other assets Total assets Liabilities: Total current liabilities Fund balance: Nonspendable Committed Assigned $2,480 0 11,848 $14,328 $11,287 1,500 0 0arrow_forward

- The following selected information was taken from SunValley City’s general fund statement of revenues, expenditures, and changes in fund balance for the year ended December 31, 2019:Revenues:Property taxes—2019 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 825,000Expenditures:Current services:Public safety . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 350,000Capital outlay (police vehicles) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100,000Debt service . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74,000Excess of revenues over expenditures . . . . . . . . . . . . . . . . . . . . $ 153,000Other financing uses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (125,000)Excess of revenues over expenditures and other financing uses. $ 28,000Decrease in fund balance assigned (encumbrances) during 2019 . 15,000Residual equity transfers-out…arrow_forwardPrepare entries in general journal form to record the following transactions in the Roadway Fund general ledger accounts for City of Kettering for the fiscal year 2018. Use modified accrual accounting. At the beginning of the fiscal year, the fund $1,360,000 was offset by the assigned fund balance in the same amount. The city was awarded $4,200,000 for road inspections and repairs during the year. The award requires reimbursement for expenditures, not an allotment upfront. Work contracted for the year amounted to $4,175,000. Invoices received for the work performed totaled $4,150,000. $3,980,000 of that amount was paid in cash as of year-end. The state reimbursed the city $4,000,000 for the completed work before year-end. Prepare a statement of Revenues, Expenditures, and Changes in Fund Balance for the Roadway Fund.arrow_forwardThe following transactions relate to the General Fund of the city of Lost Angels for the year ending December 31, 2017. Prepare a statement of revenues, expenditures, and other changes in fund balance for the general fund for the period to be included in the fund financial statements. Assume that the fund balance at the beginning of the year was $180,000. Assume also that the purchases method is applied to the supplies and that receipt within 60 days is used as the definition of avail-able resources.a. Collected property tax revenue of $700,000. A remaining assessment of $100,000 will be collected in the subsequent period. Half of that amount should be collected within 30 days, and the remainder will be received in about five months after the end of the year.b. Spent $200,000 on four new police cars with 10-year lives. A price of $207,000 had been anticipated when the cars were ordered. The city calculates all depreciation using the straight-line method with no salvage value. The…arrow_forward

- ! Required information [The following information applies to the questions displayed below.] The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2024, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund. Accounts payable Accounts receivable Accrued interest payable Accumulated depreciation Administrative and selling expenses Allowance for uncollectible accounts Capital assets Cash Charges for sales and services Cost of sales and services Depreciation expense Due from General Fund Interest expense Interest revenue Transfer in from General Fund Bank note payable Supplies inventory Totals Required A Required B Complete this question by entering your answers in the tabs below. Required C VILLAGE OF SEASIDE PINES ENTERPRISE FUND Statement of Net Position December 31, 2024 Net Position: Net Investment in Capital Assets Unrestricted Total Net Position Debits Required: a.…arrow_forwardPrepare the journal entries necessary for the following transactions. For each transaction you must identify the fund in which the entries are recorded. Make the entries only for the Fund-Based Financial Statements for the fiscal year ended 6/30/2021. 1. The board of commissioners of the Cosmo City adopted a General Fund budget for the year ending June 30, 2021, which indicated revenues of $5,100,000, bond proceeds of $620,000, appropriations of $1,900,000 for salaries, $800,000 for advertising, $400,000 for supplies, and $800,000 for utilities, and also operating transfers out of $980,000. 2. Cosmo City collected $22,000 from parking meters. 3. On March 12, 2021, Cosmo City ordered a new computer at an anticipated cost of $414,000. The computer was received on April 16 with an actual cost of $416,200. Payment was subsequently made on May 15, 2021. 4. Property taxes of 1,800,000 are levied for Cosmo City. The city expects that 5% will be uncollectible. Of the levied amount,…arrow_forwardThe following information was abstracted from the accounts of the General Fund of the City of Rome after the books had been closed for the fiscal year ended June 30, 2020. Cash Taxes Receivable Allowance for Uncollectible Taxes Accounts Payable Fund Balance View transaction llest Postclosing Trial Balance June 30, 2019 $571,600 36,000 $687,608 5,608 182,808 500,000 $607,608 Clear entry 1 Record the transfer of taxes receivable to revenues control account. 2 Record the receipt of taxes and the uncollectibles. 3 Record the expenditures payable. 4 Record the payment of expenditure. 5 Record the transfer out of general fund. Hint: This is the plug needed to make cash balance after considering the other entries. 6 Record the transfer of revenue and expenditure control accounts to fund balance. Note: = journal entry has been entered Record entry Transactions July 1, 2019, to June 30, 2020 Debits $1,370,000 1,482,488 5,600 1,387,600 X There were no transfers into the General Fund, but there…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education