a.

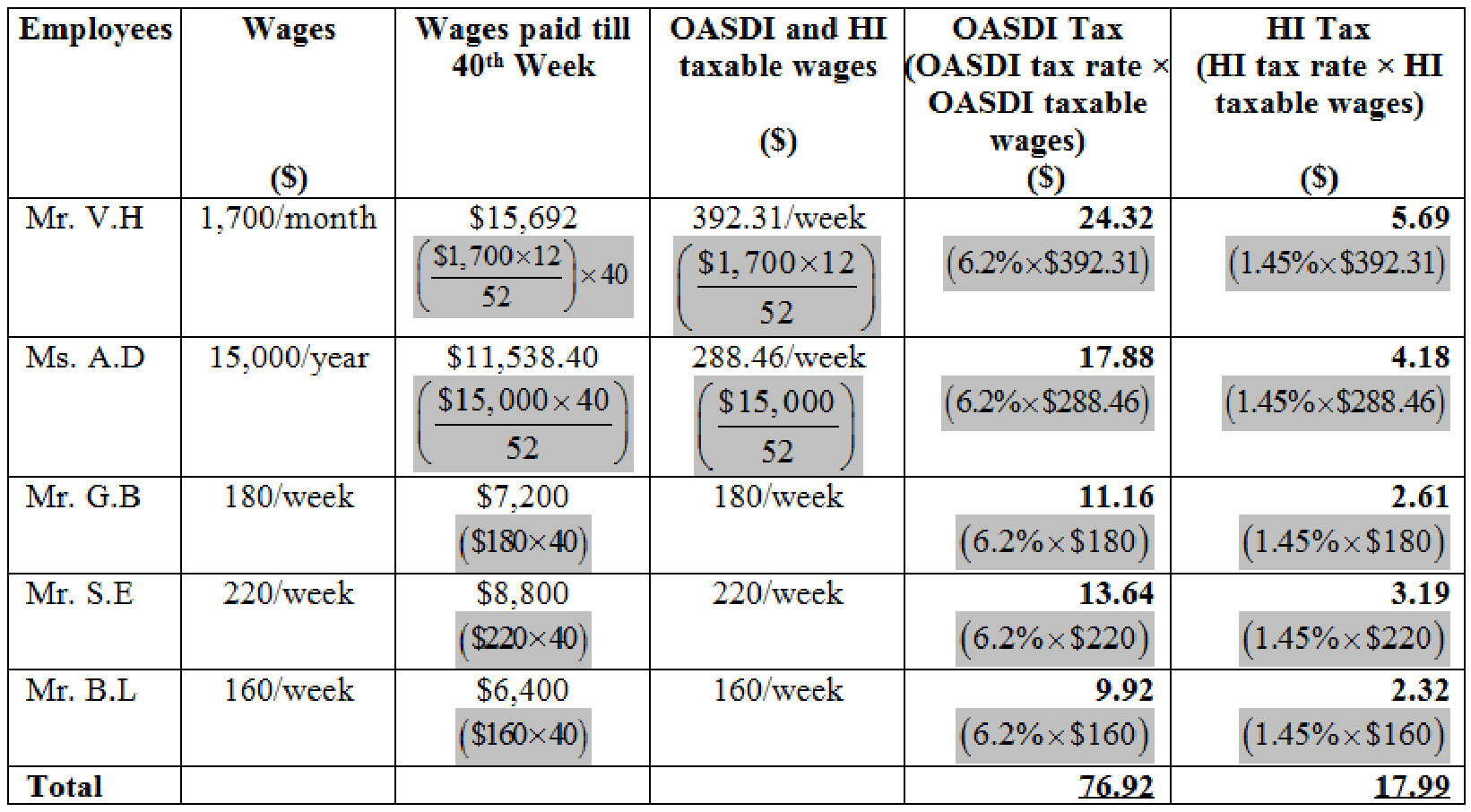

Calculate FICA tax (OASDI and HI) to be withheld for each person.

a.

Explanation of Solution

Federal Insurance Contributions Act (FICA) tax: Federal government imposes taxes on the employees’ pay to provide benefits to retired, old age, orphans, and disabled. This tax is also referred to as Social Security tax because the program is devised to benefit the society. FICA tax includes two components, OASDI (Old age, survivors, and disability insurance), and HI (health insurance).

Calculate FICA tax (OASDI and HI) to be withheld for each person.

Table (1)

Note 1: For all the employees, the wages paid till 40th Week is less than the taxable wage limit of $128,400. Hence, full weekly wages of each employee will be taxable for OASDI and HI.

Note 2: The amount received by both the partners is considered as the drawings and not a salary. Thus, FICA taxes are not imposed.

b.

Calculate the amount of the employer’s FICA taxes for the weekly payroll.

b.

Explanation of Solution

Calculate the amount of the employer’s FICA taxes for the weekly payroll.

c.

Calculate the amount of state

c.

Explanation of Solution

State unemployment compensation tax (SUTA): This is the compensation provided to the unemployed people by the state government from the taxes collected from the employers, as a percentage of 5.4% of employees’ payrolls.

Calculate the amount of state unemployment contributions for the weekly payroll.

Step 1: Compute 41st week taxable wages of employee’s for SUTA.

| Employee | Designation | Wages ($) | Wages up to 40th week ($) | Taxable wages on 41st week ($) |

| Mr. V.H | General office worker | 1,700/month |

15,692.40 |

- |

| Ms. A.D | Saleswoman | 15,000/year |

11,538.46 |

- |

| Mr. G.B | Stock clerk | 180/week |

7,200 |

180 |

| Mr. S.E | Deliveryman | 220/week |

8,800 |

- |

| Mr. B.L | Cleaning and maintenance, part-time | 160/week |

6,400 |

160 |

| Total | 340 |

Table (2)

Note 1: For Mr. V.H, Ms. A.D, and Mr. S.E, up to 40th week, the wages is crossing the limit of $8,100. So, none of the wages is taxable in 41st week.

Note 2: For Mr. G.B, up to 40th week, the wages of $7,200 is not crossing the limit of $8,100. So, the full wages of $180 is taxable in 41st week.

Note 3: For Mr. B.L, up to 40th week, the wages of $6,400 is not crossing the limit of $8,100. So, the full wages of $160 is taxable in 41st week.

Step 2: Compute the amount of state unemployment contributions for the weekly payroll.

Hence, the amount of state unemployment contributions for the weekly payroll is $10.54.

d.

Calculate net FUTA tax on the payroll.

d.

Explanation of Solution

Federal unemployment compensation tax (FUTA): This is the compensation provided to the unemployed people by the federal government from the taxes collected from the employers, as a percentage of 6.0% on the first $7,000 of employees’ earnings. Federal government refunds the employers with 5.4% on FUTA, if the employers have paid SUTA. So, FUTA would be reduced to 0.6% for those employers.

Calculate net FUTA tax on the payroll.

Step 1: Compute 41st week taxable wages of employee’s for FUTA.

| Employee | Designation | Wages ($) | Wages up to 40th week ($) | Taxable wages on 41st week ($) |

| Mr. V.H | General office worker | 1,700/month |

15,692.40 |

- |

| Ms. A.D | Saleswoman | 15,000/year |

11,538.46 |

- |

| Mr. G.B | Stock clerk | 180/week |

7,200 |

- |

| Mr. S.E | Deliveryman | 220/week |

8,800 |

- |

| Mr. B.L | Cleaning and maintenance, part-time | 160/week |

6,400 |

160 |

| Total | 160 |

Table (3)

Note 1: For Mr. V.H, Ms. A.D, Mr. GB, and Mr. S.E, up to 40th week, the wages is crossing the limit of $7,000. So, none of the wages is taxable in 41st week.

Note 3: For Mr. B.L, up to 40th week, the wages of $6,400 is not crossing the limit of $7,000. So, the full wages of $160 is taxable in 41st week.

Step 2: Calculate net FUTA tax.

Hence, the net FUTA tax on the payroll is $0.96.

e.

Calculate the total amount of employer’s payroll taxes for the weekly payroll.

e.

Explanation of Solution

| Calculation of employer’s payroll taxes | |

| Type of Tax | Tax Amount |

| OASDI | $76.92 |

| HI | $17.99 |

| FUTA | $0.96 |

| SUTA | $10.54 |

| Total employer’s payroll taxes | $106.41 |

Table (4)

Hence, the total amount of employer’s payroll taxes for the weekly payroll is $106.41.

Want to see more full solutions like this?

Chapter 5 Solutions

PAYROLL ACCT.,2019 ED.(LL)-TEXT

- Audrey Martin and Beth James are partners in the Country Gift Shop, which employs the individuals listed below. Paychecks are distributed every Friday to all employees. Based on the information given, compute the amounts listed below for a weekly payroll period. Employers OASDI Tax ________ Employers HI Tax ________arrow_forwardPayrex Co. has six employees. All are paid on a weekly basis. For the payroll period ending January 7, total employee earnings were 12,500, all of which were subject to SUTA, FUTA, Social Security, and Medicare taxes. The SUTA tax rate in Payrexs state is 5.4%, but Payrex qualifies for a rate of 2.0% because of its good record of providing regular employment to its employees. Other employer payroll taxes are at the rates described in the chapter. REQUIRED 1. Calculate Payrexs FUTA, SUTA, Social Security, and Medicare taxes for the week ended January 7. 2. Prepare the journal entry for Payrexs payroll taxes for the week ended January 7. 3. What amount of payroll taxes did Payrex save because of its good employment record?arrow_forwardToren Inc. employs one person to run its solar management company. The employee’s gross income for the month of May is $6,800. Payroll for the month of May is as follows: FICA Social Security tax rate at 6.2%, FICA Medicare tax rate at 1.45%, federal income tax of $450, state income tax of $95, health-care insurance premium of $210, and union dues of $50. The employee is responsible for covering 30% of his or her health insurance premium. A. Record the journal entry to recognize employee payroll for the month of May, dated May 31, 2017. Round your answers to the nearest whole dollar. If an amount box does not require an entry, leave it blank. May 31 fill in the blank ae540107305b069_2 fill in the blank ae540107305b069_3 fill in the blank ae540107305b069_5 fill in the blank ae540107305b069_6 fill in the blank ae540107305b069_8 fill in the blank ae540107305b069_9 fill in the blank ae540107305b069_11 fill in the blank ae540107305b069_12 fill in the…arrow_forward

- Frances Newberry is the payroll accountant for Pack-It Services of Jackson, Arizona. The employees of Pack-It Services are paid semimonthly. An employee, Glen Riley, comes to her on November 6 and requests a pay advance of $1,650, which he will pay back in equal parts on the November 15 and December 15 paychecks. Glen is married with eight withholding allowances and is paid $58,640 per year. He contributes 3 percent of his pay to a 401(k) and has $25 per paycheck deducted for a Section 125 plan. Compute his net pay on his November 15 paycheck. The applicable state income tax rate is 2.88 percent. Use the Wage Bracket Method Tables for Income Tax Withholding in Appendix C. (Round your intermediate calculations and final answer to 2 decimal places.)arrow_forwardDeep Mouse Designs has 14 employees within Denver City and County. The employees earned $9.80 per hour and worked 160 hours each during the month. The employer must remit $4.00 per month per employee who earns more than $500 per month. Additionally, employees who earn more than $500 per month must have $5.75 withheld from their pay. Required: What is the employee and employer Occupational Privilege Tax for these employees? (Round your answers to 2 decimal places.)arrow_forwardIn Oregon, employers who are covered by the state workers' compensation law withhold employee contributions from the wages of covered employees for the workers' benefit fund at the rate of 1.2¢ for each hour or part of an hour that the worker is employed. Every covered employer is also assessed 1.2¢ per hour for each worker employed for each hour or part of an hour. The employer-employee contributions for workers' compensation are collected monthly, quarterly, or annually by the employer's insurance carrier, according to a schedule agreed upon by the employer and the carrier. The insurance carrier remits the contributions to the state's Workers' Compensation Department. Cortez Company, a covered employer in Oregon, turns over the employer-employee workers' compensation contributions to its insurance carrier by the 15th of each month for the preceding month. During the month of July, the number of full-time employee-hours worked by the company's employees was 8,490; the number of…arrow_forward

- Toren Inc. employs one person to run its solar management company. The employee's gross income for the month of May is $6,800. Payroll for the month of May is as follows: FICA Social Security tax rate at 6.2%, FICA Medicare tax rate at 1.45%, federal income tax of $410, state income tax of $80, health-care insurance premium of $240, and union dues of $70. The employee is responsible for covering 30% of his or her health insurance premium. A. Record the journal entry to recognize employee payroll for the month of May, dated May 31, 2017. Round your answers to the nearest whole dollar. If an amount box does not require an entry, leave it blank. May 31 B. Record remittance of the employee's salary with cash on June 1. Round your answers to the nearest whole dollar. If an amount box does not require an entry, leave it blank. June 1arrow_forwardR.D. Kagen employs Audrey Lopez at a salary of $33,800 a year. Kagen is subject to employer Social Security taxes at a rate of 6.2% and Medicare taxes at a rate of 1.45% on Lopez's salary. In addition, Kagen must pay SUTA tax at a rate of 5.4% and FUTA tax at a rate of 0.6% on the first $7,000 of Lopez's salary. Compute the total cost to Kagen of employing Lopez for the year. $arrow_forwardR.D. Kagen employs Audrey Lopez at a salary of $33,800 a year. Kagen is subject to employer Social Security taxes at a rate of 6.2% and Medicare taxes at a rate of 1.45% on Lopez's salary. In addition, Kagen must pay SUTA tax at a rate of 5.4% and FUTA tax at a rate of 0.6% on the first $7,000 of Lopez's salary. Compute the total cost to Kagen of employing Lopez for the year. If required, round your answer to the nearest cent.arrow_forward

- Toren Inc. employs one person to run its solar management company. The employee's gross income for the month of May is $7,208. Payroll for the month of May is as follows: • FICA Social Security tax rate at 6.2% FICA Medicare tax rate at 1.45% Federal income tax of $400 • State income tax of $75 Health-care insurance premium of $298 • Union dues of $50 • The employee is responsible for covering 14% of his or her health insurance premium What is the net pay of the one employee for the month of May? Round to the nearest penny, two decimals. # No new data to save. Last checked at 11:47pm Submit Carrow_forwardR. L. Ybarra employs John Ince at a salary of $53,000 a year. Ybarra is subject to employer Social Security taxes at a rate of 6.2% and Medicare taxes at a rate of 1.45% on John's salary. In addition, Ybarra must pay SUTA tax at a rate of 5.4% and FUTA tax at a rate of 0.8% on the first $7,000 of Ince's salary. Compute the total cost to Ybarra of employing Ince for the year. Round your answer to the nearest cent.arrow_forwardMarbury is the payroll accountant at All's Fair Gifts. The employees of All's Fair Gifts are paid semimonthly. Sten comes to Marbury on April 7 and requests a pay advance of $1,000, which Sten will pay back in equal parts on the April 15 and May 15 paychecks. Sten is single, with one dependent under 17, is paid $57,200 per year, contributes 3 percent of gross pay to a 401(k), and has $134 per paycheck deducted for a Section 125 plan. Required: Compute the net pay on Sten's April 15 paycheck. The applicable state income tax rate is 5.25 percent. Use the wage-bracket method for manual payroll systems with Forms W-4 from 2020 or later in Appendix C to determine the federal income tax. Assume box 2 is not checked. Note: Round your intermediate calculations and final answer to 2 decimal places. Net payarrow_forward

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,