EBK INTERMEDIATE MICROECONOMICS AND ITS

12th Edition

ISBN: 9781305176386

Author: Snyder

Publisher: YUZU

expand_more

expand_more

format_list_bulleted

Question

Chapter 1A.5, Problem 1TTA

To determine

To explain the operation of OPEC in term of

Expert Solution & Answer

Explanation of Solution

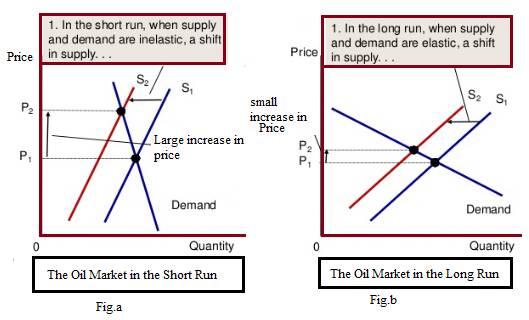

The following figure shows the effects on supply and demand:

In the case of the oil market, when supply decreases, the response depends on the time horizon. The operation of OPEC varies in the short-run and in the long run.

Fig A. shows that when the demand and supply is inelastic, then the shift in supply curve (S1 to S2) leads to a greater increase in price.

However, in the long run, when supply and demand is elastic, then shift in supply curve (S1 to S2) in fig b. leads to a small increase in price (P1 to P2). Thus, in the shortrun, the price increases to at a greater degree as compared to the long run.

Want to see more full solutions like this?

Subscribe now to access step-by-step solutions to millions of textbook problems written by subject matter experts!

Students have asked these similar questions

Suppose that the world price of oil is roughly

$90.00 per barrel and that the world demand and

total world supply of oil equal 34 billion barrels per

year (bb/yr), with a competitive supply of 20 bb/yr

and 14 bb/yr from OPEC. Statistical studies have

shown that the long-run price elasticity of

demand for oil is -0.40, and the long-run

competitive price elasticity of supply is 0.40.

Using this information, derive linear demand and

competitive supply curves for oil.

Let the demand curve be of the general form

Q=a-bP

and the competitive supply curve be of the

general form

Q=c+dP,

where a, b, c, and d are constants.

The equation for the long-run demand curve is

A.Q=47.50-0.15P.

B.Q=13.50-47.50P.

C.Q=47.50-P.

D.Q=47.50+0.15P.

E.Q=13.50-0.15P.

The opening statement on the website of the Organization of Petroleum Exporting Countries (OPEC) says its members seek “ … to secure an efficient, economic and regular supply of petroleum to consumers, a steady income to producers and a fair return on capital for those investing in the petroleum industry.” To achieve these goals, OPEC attempts to coordinate and unify petroleum policies by raising or lowering its members’ collective oil production. However, increased production by the United States, Russia, Oman, Mexico, Norway, and other non-OPEC countries has placed downward pressure on the price of crude oil.

Please explain:

To achieve these goals of stable and fair oil prices, what must OPEC do to maintain the price of oil at its desired level?

How easy is it for OPEC to achieve this goal?

Suppose that the world price of oil is roughly $50.00 per barrel and that the world demand and total world supply of oil equal 34 billion barrels per year (bb/yr), with a competitive supply of 20 bb/yr and 14 bb/yr from OPEC.

Statistical studies have shown that the long-run price elasticity f demand for oil is -0.40, and the long-run competitive price elasticity of supply is 0.40. Using this information, derive linear demand and competitive

supply curves for oil.

Let the demand curve be of the general form Q = a - bP and the competitive supply curve be of the general form Q = c+dP, where a, b, c, and d are constants.

The equation for the long-run demand curve is

O A. Q=47.50 -0.27P.

O B. Q=13.50 -0.27P.

OC. Q=47.50-P

O D. Q=47.50+ 0.27P.

O E. Q=13.50-47.50P.

The equation for the long-run competitive supply curve is

O A. Q=12.00 + 47.50P.

OB. Q=12.00 -0.16P.

OC. Q 8.00+ 0.16P.

O D. Q=8.00+ 0.27P.

O E. Q=12.00 +0.16P.

Chapter 1A Solutions

EBK INTERMEDIATE MICROECONOMICS AND ITS

Knowledge Booster

Similar questions

- Suppose that the world demand and supply elasticities of crude oil are -0.906 and 0.515, respectively. The current equilibrium price is $30 per barrel and the equilibrium quantity is 16.88 billion barrels per year. Derive the linear demand and supply equations. Now suppose the world supply curve you derived above consists of competitive supply and OPEC supply. If the competitive supply equation is: SC = 7.78 + 0.29P, what must be OPEC's level of production in this equilibrium? Now suppose social and political unrest in some non-OPEC producing countries reduced the competitive supply by 30 percent, what happens to the world price of crude oil?arrow_forwardConsider a hypothetical world consisting of only three countries: Hungary, Australia, and Italy. Each country produces grain. Hungary is a small economy compared to Australia and Italy and thus cannot influence foreign prices. On the following graph, the supply and demand schedules of Hungary are shown as Sun and Dun. Foreign supply schedules of grain are perfectly elastic: Australia is a more efficient supplier of grain than Italy because its supply price is $1.00 per bushel (SAus), whereas Italy's supply price is $2.00 per bushel (Sita). PRICE (Dollars) 10.00 9.00 8.00 7.00 6.00 5.00 4.00 3.00 2.00 1.00 0 Hun S +T S₁ +T S S + 0 3 6 A Scenario Free trade With tariff With customs union m SHu 12 15 18 21 24 27 30 GRAIN (Thousands of bushels) Calculate the quantity of bushels Hungary imports when the three nations engage in free trade. Enter this value in the first row of the following table. Also indicate which country Hungary imports from. ? Imports (Thousands of bushels) Imports…arrow_forwardCountry C imports 80,000 metric tons of steel from Country U and produces domestically 80,000 metric tons per year. The world price of steel is $500 per metric ton. Assuming linear schedules, research analysts estimated the price elasticity of domestic supply to be 0.50 and the price elasticity of domestic demand to be -0.25 in the current market equilibrium. Country C imposes an import duty of $150 per metric ton that caused the world price to fall by 10%. Analyse the effects of the consumer surplus, producer surplus, government revenue, and deadweight loss in the Country C steel market with the tariff. What are the terms of trade of the Country C steel market after the tariff was imposed? Explain the welfare effects of both countries.arrow_forward

- Country C imports 80,000 metric tons of steel from Country U and produces domestically 80,000 metric tons per year. The world price of steel is $500 per metric ton. Assuming linear schedules, research analysts estimated the price elasticity of domestic supply to be 0.50 and the price elasticity of domestic demand to be -0.25 in the current market equilibrium. Country C imposes an import duty of $150 per metric ton that caused the world price to fall by 10%. Summarise and analyse the quantity of steel produced, consumed and imported in Country C. Analyse and discuss the welfare gain from trade in Country C. Show your answers of the steel market with a proper diagram. Imports steel from Country U = 80,000 metric tons of steel Produce domestically = 80,000 metric tons per year Country C total steel consumption = 160,000 metric tons per year Price of steel per metric ton = $500arrow_forwardCountry C imports 80,000 metric tons of steel from Country U and produces domestically 80,000 metric tons per year. The world price of steel is $500 per metric ton. Assuming linear schedules, research analysts estimated the price elasticity of domestic supply to be 0.50 and the price elasticity of domestic demand to be -0.25 in the current market equilibrium. Country C imposes an import duty of $150 per metric ton that caused the world price to fall by 10%. (a) Summarise and analyse the quantity of steel produced, consumed and imported in Country C. Analyse and discuss the welfare gain from trade in Country C. Show your answers of the steel market with a proper diagram. (b) Analyse the effects of the consumer surplus, producer surplus, government revenue and deadweight loss in the Country C steel market with the tariff. What are the terms of trade of the Country C steel market after the tariff was imposed? Explain the welfare effects of both countries.arrow_forwardCountry C imports 80,000 metric tons of steel from Country U and produces domestically 80,000 metric tons per year. The world price of steel is $500 per metric ton. Assuming linear schedules, research analysts estimated the price elasticity of domestic supply to be 0.50 and the price elasticity of domestic demand to be -0.25 in the current market equilibrium. Country C imposes an import duty of $150 per metric ton that caused the world price to fall by 10%. Summarise and analyze the quantity of steel produced, consumed, and imported in Country C. Analyse and discuss the welfare gain from trade in Country C. Show your answers to the steel market with a proper diagram.arrow_forward

- In mid-2010, Saudi Arabia and Venezuela (both members of OPEC) produced an average of 8 million and 3 million barrels of oil a day, respectively. Production costs were about $20 per barrel, and the price of oil averaged $80 per barrel. Each country had the capacity to produce an extra 1 million barrels per day. At that time, it was estimated that each 1-million-barrel increase in supply would depress the average price of oil by $10. Consider the competition between Saudi Arabia and Venezuela as a game. a) Construct the payoff table. b) Do countries have a dominant strategy? c) What actions should each country take and why?arrow_forwardThe oversupply of bananas in Mexico, which is recorded in the months of September and October, causes prices to farmers to be reduced by up to 50 percent below the cost of production, said Adrián Prats, president of the banana product system at the national. "It is a critical situation, we are selling the fruit below the cost of production, which is when it really impacts the producer, since he has to continue maintaining his plantations healthy and vigorous and that costs. We have to invest in it, even though the price is not giving to pay, even, the costs", explained Prats. The above causes: a. By decreasing the price of bananas, marginal income decreases and therefore, production must be increased (T/F) _________ b. By lowering the price, the company will have to take care of its costs. To avoid leaving the market, the producer must ensure that, at least, the average variable costs (T/F) _______ are covered c. It is recommended that a banana producer who invests in keeping his…arrow_forwardWhat can you say about the degree of impact that tourism has on our societyarrow_forward

- How can GM maintain control of its production in the China market?arrow_forwardNiama Oil Wells, owned by the Nigerian government, have decided to export oil from its oil wells to the high-income countries. Which of the following countries is ideal for its export strategy? A) Kazakhstan B) Algeria C) China D) the United States E) Argentinaarrow_forwardWe typically focus on firms from well-developed economies entering markets of less developed economies. Do firms from less developed economies have a chance of success if they enter developed markets, such as the United States? What competitive advantage could a firm from a less developed economy rely on in entering developed markets? What would likely be the best entry mode?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education