Concept explainers

Videos

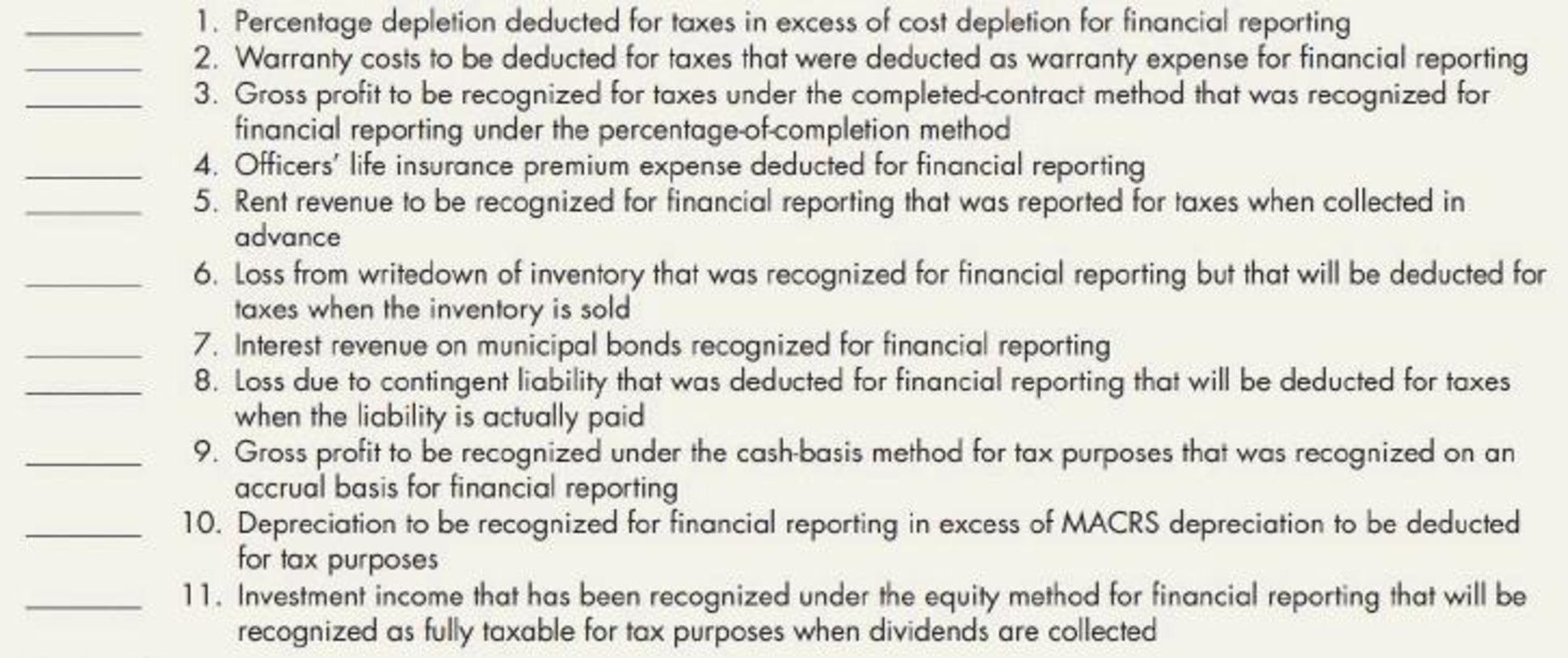

Temporary and Permanent Differences In the current year, you are calculating a diversified company’s

Required:

For each difference, indicate whether it is a temporary difference (T) or a permanent difference (P) by placing the appropriate letter on the line provided. If the difference is a temporary difference, also indicate for the current year whether it will result in a future taxable amount (FT) or a future deductible amount (FD).

Trending nowThis is a popular solution!

Chapter 18 Solutions

Intermediate Accounting: Reporting And Analysis

Additional Business Textbook Solutions

Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

Horngren's Financial & Managerial Accounting, The Financial Chapters (6th Edition)

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Cost Accounting (15th Edition)

PRINCIPLES OF TAXATION F/BUS.+INVEST.

Managerial Accounting: Tools for Business Decision Making

- Definitions The FASB has defined several terms in regard to accounting for income taxes. Below are various code letters (for terms) followed by definitions. 1. The deferred tax consequences of future deductible amounts and operating loss carryforwards 2. A difference between the tax basis of an asset or liability and its reported amount in the financial statements that will result in taxable or deductible amounts in future years when the reported amount of the asset or liability is recovered or settled, respectively 3. Temporary difference that results in taxable amounts in future years when the related asset or liability is recovered or settled, respectively 4. The future effects on income taxes, as measured by the applicable enacted tax rate and provisions of the enacted tax low, resulting from temporary differences and operating loss carryforwards at the end of the current year 5. The change during the year in a corporations deferred tax liabilities and assets 6. The deferred tax consequences of future taxable amounts 7. The portion of o deferred tax asset for which it is more likely than not that a tax benefit will not be realized 8. Temporary difference that results in deductible amounts in future years when the related asset or liability is recovered or settled, respectively 9. The sum of income tax payable and deferred tax expense (or benefit) 10. The amount of income taxes paid or payable (or refundable) for the current year 11. An excess of tax deductible expenses over taxable revenues in a year that may be carried forward to reduce taxable income in a future year 12. The excess of taxable revenues over tax deductible expenses and exemptions for the year 13. Income tax expense divided by income before income taxesarrow_forwardWhen a company pays taxes that were previously recorded as a deferred tax liability, the temporary difference ________. Group of answer choices decreases reverses increases originatesarrow_forward1. Which of the following statements is incorrect regarding deferred taxes? a. Income tax payable plus or minus the change in deferred income taxes equals total income tax expense. b. The deferred portion of income tax expense is the amount of change in deferred taxes related to the current period. c. In computing income tax expense, a company deducts an increase in a deferred tax liability to income tax payable. d. All of the choices are incorrect. 2. A liability in 2021 is reported for financial reporting purposes but not for tax purposes. When this liability is settled in 2022, a future taxable amount will: a. pretax financial income will exceed taxable income in 2022. b. the Company will record a decrease in a deferred tax liability in 2022. c. total income tax expense for 2022 will exceed current tax expense for 2022. d. will not be affected. 3. Assuming a 35% statutory tax rate applies to all years involved, which of the following situations will give rise to reporting a…arrow_forward

- Which general principle applies to the reporting of income tax expenses under interim income statement accounting principles A Reporting should not be done unless there are unusual events that occur in the period and are expect to affect the fiscal year tax liability. B Reporting should be based on a prorate share of the previous fiscal year’s taxes C Reporting should be based on an estimate of the effective annual tax rate and tax liability for the full fiscal year. D Reporting should be based on the last year’s effective tax rates and tax liability for the full fiscal year.arrow_forwardTo calculate the company's income tax expense for the current period, it is necessary to know: Multiple Choice the company's operating revenue and tax bill from prior periods. the company's income before income taxes and the company's tax rate. the company's operating expenses and revenue. the company's net income from the previous period and the current tax rate.arrow_forwardUnder IFRS when a change in the tax rates is enacted I. Companies should record its effect on existing deferred tax accounts immediately. II. Companies report the effect of changes in tax rates on deferred tax accounts in the period the new rate becomes effective. III. Companies report the effect of changes in tax rates on deferred tax accounts that arise in future periods when the new tax rates are in effect. Select one: a. Either I, II, or III, depending on how frequently tax rates change in the company’s tax jurisdiction b. II Only c. I Only d. III Onlyarrow_forward

- Tax rates other than the current tax rate may be used to calculate the deferred income tax amount for financial statement reporting if O it is probable that a future tax rate change will occur. O it appears likely that a future tax rate will be greater than the current tax rate. O it appears likely that a future tax rate will be less than the current tax rate. O the enacted tax rate is expected to apply in future years.arrow_forwardRequired: 1. Prepare the journal entry to recognize the income tax benefit of the net operating loss in 2021. Assume Fore will carry back its NOL to prior years. 2. What is the net operating loss reported in 2021 income statement? 3. Prepare the journal entry to record income taxes in 2022 assuming pretax accounting income is $288 million. No additional temporary differences originate in 2022.arrow_forwardA reduction in the statutory tax rate would most likely benefi t the company’s:A . income statement and balance sheet.B . income statement but not the balance sheet.C . balance sheet but not the income statement.arrow_forward

- Refund of value added taxes in the current year which were erroneously paid in a prior year is generally Subject to final income tax Included in gross income O Not included in gross income O Deducted from retained earningsarrow_forwardWhich of the following is not a cause of a difference between pretax financial income and taxable income in a given period? a. operating loss carryforwards b. permanent differences c. applicable tax rates d. temporary differencesarrow_forwardInterperiod Tax Allocation Klerk Company had four temporary differences between its pretax financial income and its taxable income during 2019 as follows: At the beginning of 2019, Klerk had a deferred tax liability of 84,300 related to Temporary Difference #2 and a deferred tax asset of 21,090 related to Temporary Difference #4. Based on its tax records, Klerk earned taxable income of 270,000 for 2019. Kerks accountant has prepared the following schedule showing the total future taxable and deductible amounts at the end of 2019 for its four temporary differences: The company has a history of earning income and expects to be profitable in the future. The income tax rate for 2019 is 40%, but in 2018 Congress enacted a 30% tax rate for 2020 and future years. During 2019, for financial accounting purposes, Klerk reported revenues of 750,000 and expenses of 447,100. The deferred taxes related to Temporary Differences #1, #2, and #4 are considered to be noncurrent by the company; the deferred tax related to Temporary Difference #3 is considered to be current. Required: 1. Prepare Klerks income tax journal entry for 2019. 2. Prepare a condensed 2019 income statement for Klerk. 3. Show how the income tax items are reported on Klerks December 31, 2019, balance sheet.arrow_forward

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning