Concept explainers

Videos

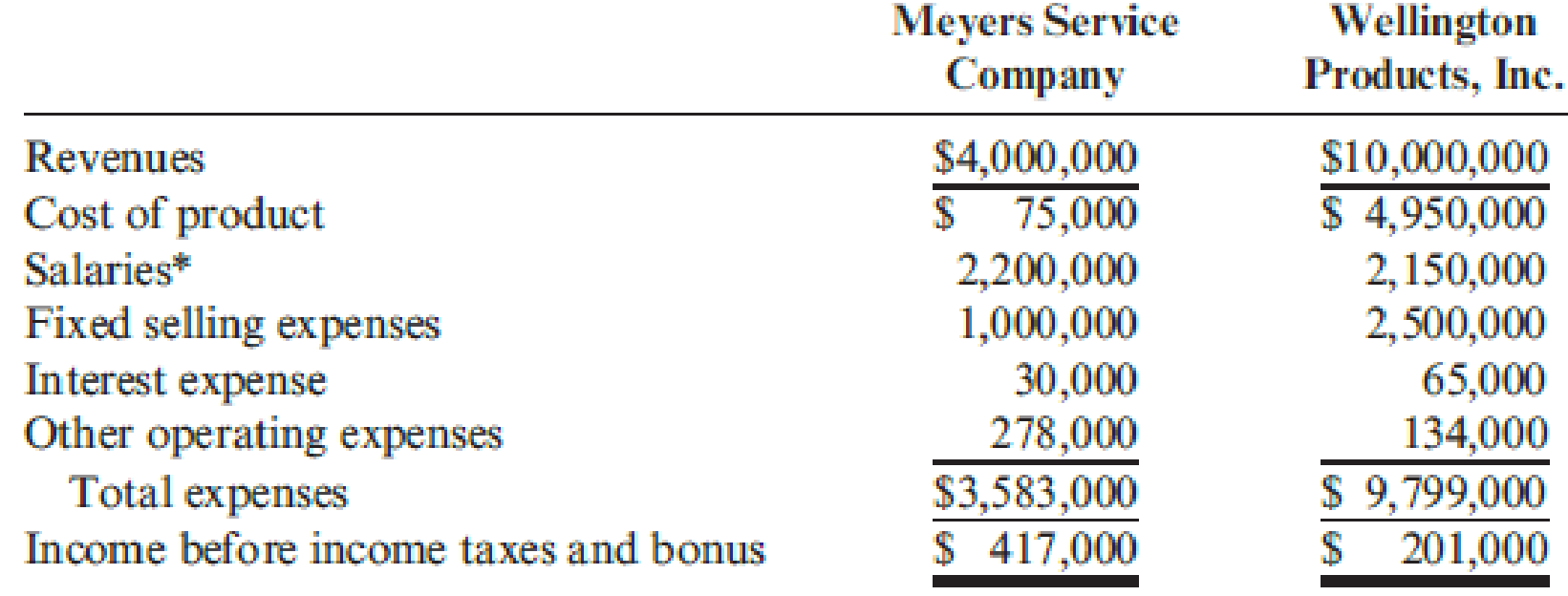

Renslen, Inc., a truck manufacturing conglomerate, has recently purchased two divisions: Meyers Service Company and Wellington Products, Inc. Meyers provides maintenance service on large truck cabs for 10-wheeler trucks, and Wellington produces air brakes for the 10-wheeler trucks.

The employees at Meyers take pride in their work, as Meyers is proclaimed to offer the best maintenance service in the trucking industry. The management of Meyers, as a group, has received additional compensation from a 10 percent bonus pool based on income before income taxes and bonus. Renslen plans to continue to compensate the Meyers management team on this basis as it is the same incentive plan used for all other Renslen divisions, except for the Wellington division.

Wellington offers a high-quality product to the trucking industry and is the premium choice even when compared to foreign competition. The management team at Wellington strives for zero defects and minimal scrap costs; current scrap levels are at 2 percent. The incentive compensation plan for Wellington management has been a 1 percent bonus based on gross margin. Renslen plans to continue to compensate the Wellington management team on this basis. The following condensed income statements are for both divisions for the fiscal year ended May 31, 20x1:

Renslen, Inc. Divisional Income Statements For the Year Ended May 31, 20x1

*Each division has $1,000,000 of management salary expense that is eligible for the bonus pool.

Renslen has invited the management teams of all its divisions to an off-site management workshop in July where the bonus checks will be presented. Renslen is concerned that the different bonus plans at the two divisions may cause some heated discussion.

Required:

- 1. Determine the 20x1 bonus pool available for the management team at:

- a. Meyers Service Company

- b. Wellington Products, Inc.

- 2. Identify at least two advantages and disadvantages to Renslen, Inc., of the bonus pool incentive plan at:

- a. Meyers Service Company

- b. Wellington Products, Inc.

- 3. Having two different types of incentive plans for two operating divisions of the same corporation can create problems.

- a. Discuss the behavioral problems that could arise within management for Meyers Service Company and Wellington Products, Inc., by having different types of incentive plans.

- b. Present arguments that Renslen, Inc., can give to the management teams of both Meyers and Wellington to justify having two different incentive plans.

Trending nowThis is a popular solution!

Chapter 10 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Magna is a company that carries out many different activities. It is proud of its reputation as a “caring” organization and has adopted various ethical policies towards its employees and the wider community in which it operates. As part of its annual financial statements, the company publishes details of its environmental policies, which include setting performance targets for activities such as recycling, controlling emissions of noxious substances and limiting use of non-renewable resources. The company has an overseas operation that is involved in mining precious metals. These activities cause significant damage to the environment, including deforestation. On April 1, 2014, the company incurred capital cost of $100 million in respect of the mine and it is expected that the mine will be abandoned in eight years’ time. The mine is situated in a country where there is no environmental legislation obliging companies to rectify environmental damage and is it very unlikely that any such…arrow_forwardMagna is a company that carries out many different activities. It is proud of its reputation as a “caring” organization and has adopted various ethical policies towards its employees and the wider community in which it operates. As part of its annual financial statements, the company publishes details of its environmental policies, which include setting performance targets for activities such as recycling, controlling emissions of noxious substances and limiting use of non-renewable resources. The company has an overseas operation that is involved in mining precious metals. These activities cause significant damage to the environment, including deforestation. On April 1, 2014, the company incurred capital cost of $100 million in respect of the mine and it is expected that the mine will be abandoned in eight years’ time. The mine is situated in a country where there is no environmental legislation obliging companies to rectify environmental damage and is it very unlikely that any such…arrow_forwardFusion Metals Company is considering the elimination of its Packaging Department. Management has received an offer from an outside firm to supply all Fusion’s packaging needs. To help her in making the decision, Fusion’s president has asked the controller for an analysis of the cost of running Fusion’s Packaging Department. Included in that analysis is $9,100 of rent, which represents the Packaging Department’s allocation of the rent on Fusion’s factory building. If the Packaging Department is eliminated,the space it used will be converted to storage space. Currently Fusion rents storage space in a nearby warehouse for $11,000 per year. The warehouse rental would no longer be necessary if the Packaging Department were eliminated. Required:1. Discuss each of the figures given in the exercise with regard to its relevance in the departmentclosing decision.2. What type of cost is the $11,000 warehouse rental, from the viewpoint of the costs of the Packaging Department?arrow_forward

- Phoenix Inc., a cellular communication company, has multiple business units, organized as divisions. Each division’s management is compensated based on the division’s operating income. Division A currently purchases cellular equipment from outside markets and uses it to produce communication systems. Division B produces similar cellular equipment that it sells to outside customers—but not to division A at this time. Division A’s manager approaches division B’s manager with a proposal to buy the equipment from division B. If it produces the cellular equipment that division A desires, division B will incur variable manufacturing costs of $60 per unit. Relevant Information about Division B Sells 90,000 units of equipment to outside customers at $130 per unit Operating capacity is currently 80%; the division can operate at 100% Variable manufacturing costs are $70 per unit Variable marketing costs are $8 per unit Fixed manufacturing costs are $900,000 Income per Unit for Division A…arrow_forwardMagna is a company that carries out many different activities. It is proud of its reputation as a “caring” organization and has adopted various ethical policies towards its employees and the wider community in which it operates. As part of its annual financial statements, the company publishes details of its environmental policies, which include setting performance targets for activities such as recycling, controlling emissions of noxious substances and limiting use of non-renewable resources. The company has an overseas operation that is involved in mining precious metals. These activities cause significant damage to the environment, including deforestation. On April 1, 2014, the company incurred capital cost of $100 million in respect of the mine and it is expected that the mine will be abandoned in eight years’ time. The mine is situated in a country where there is no environmental legislation obliging companies to rectify environmental damage and is it very unlikely that any such…arrow_forwardSpeed Racer in Victoria makes bicycles for people of all ages. The frames division makes and paints the frames and supplies them to the assembly division where the bicycles are assembled. Speed Racer is a successful and profitable corporation that attributes much of its success to its decentralized operating style. Each division manager is compensated on the basis of division operating income. The assembly division currently acquires all its frames from the frames division. The assembly division manager could purchase similar frames in the market for $480. The frames division is currently operating at 80% of its capacity of 4,000 frames (units) and has the following details: Voltage Regulator Direct materials ($150 per unit x 320 units) $480,000 Direct manufacturing labour ($60 per unit x 3,200 units) 192,000 Variable manufacturing overhead costs ($30 per unit × 3,200 units) 96,000 Fixed manufacturing overhead costs $624,000 All the frames division’s…arrow_forward

- Speed Racer in Victoria makes bicycles for people of all ages. The frames division makes and paints the frames and supplies them to the assembly division where the bicycles are assembled. Speed Racer is a successful and profitable corporation that attributes much of its success to its decentralized operating style. Each division manager is compensated on the basis of division operating income. The assembly division currently acquires all its frames from the frames division. The assembly division manager could purchase similar frames in the market for $480. The frames division is currently operating at 80% of its capacity of 4,000 frames (units) and has the following details: Voltage Regulator Direct materials ($150 per unit x 320 units) $480,000 Direct manufacturing labour ($60 per unit x 3,200 units) 192,000 Variable manufacturing overhead costs ($30 per unit × 3,200 units) 96,000 Fixed manufacturing overhead costs $624,000 All the frames division’s…arrow_forwardSpeed Racer in Victoria makes bicycles for people of all ages. The frames division makes and paints the frames and supplies them to the assembly division where the bicycles are assembled. Speed Racer is a successful and profitable corporation that attributes much of its success to its decentralized operating style. Each division manager is compensated on the basis of division operating income. The assembly division currently acquires all its frames from the frames division. The assembly division manager could purchase similar frames in the market for $480. The frames division is currently operating at 80% of its capacity of 4,000 frames (units) and has the following details: Voltage Regulator Direct materials ($150 per unit x 320 units) $480,000 Direct manufacturing labour ($60 per unit x 3,200 units) 192,000 Variable manufacturing overhead costs ($30 per unit × 3,200 units) 96,000 Fixed manufacturing overhead costs $624,000 All the frames division’s…arrow_forwardSpeed Racer in Victoria makes bicycles for people of all ages. The frames division makes and paints the frames and supplies them to the assembly division where the bicycles are assembled. Speed Racer is a successful and profitable corporation that attributes much of its success to its decentralized operating style. Each division manager is compensated on the basis of division operating income. The assembly division currently acquires all its frames from the frames division. The assembly division manager could purchase similar frames in the market for $480. The frames division is currently operating at 80% of its capacity of 4,000 frames (units) and has the following details: Voltage Regulator Direct materials ($150 per unit x 320 units) $480,000 Direct manufacturing labour ($60 per unit x 3,200 units) 192,000 Variable manufacturing overhead costs ($30 per unit × 3,200 units) 96,000 Fixed manufacturing overhead costs $624,000 All the frames…arrow_forward

- Speed Racer in Victoria makes bicycles for people of all ages. The frames division makes and paints the frames and supplies them to the assembly division where the bicycles are assembled. Speed Racer is a successful and profitable corporation that attributes much of its success to its decentralized operating style. Each division manager is compensated on the basis of division operating income. The assembly division currently acquires all its frames from the frames division. The assembly division manager could purchase similar frames in the market for $480. The frames division is currently operating at 80% of its capacity of 4,000 frames (units) and has the following details: Voltage Regulator Direct materials ($150 per unit x 320 units) $480,000 Direct manufacturing labour ($60 per unit x 3,200 units) 192,000 Variable manufacturing overhead costs ($30 per unit × 3,200 units) 96,000 Fixed manufacturing overhead costs $624,000 All the frames…arrow_forwardClonal Inc., a biotechnology company, developed and patented a diagnostic product called Trouver. Clonal purchased some research equipment to be used exclusively for Trouver and other research equipment to be used on Trouver and subsequent research projects. Clonal defeated a legal challenge to its Trouver patent and began production and marketing operations for the product. Clonal allocated its corporate headquarters’ costs to its research division as a percentage of the division’s salaries. Required: What is the definition of research and of development as defined by GAAP? Briefly indicate the justification for the existing GAAP relating to R&D costs. Explain how Clonal should report the equipment purchased for Trouver on its income statements and balance sheets. Explain how Clonal should report the legal costs incurred in defending Trouver’s patent on its statement of cash flows. Explain how Clonal should classify its corporate headquarters’ costs allocated to the…arrow_forwardLenox Manufacturing Co. produces and sells specialized equipment used in the petroleum industry. The company is organized into three separate operating branches: Division A, which manufactures and sells heavy equipment; Division B, which manufactures and sells hand tools; and Division C, which makes and sells electric motors. Each division is housed in a separate manufacturing facility. Company headquarters is located in a separate building. In recent years, Division B has been operating at a net loss and is expected to continue to do so. Income statements for the three divisions for year 2 follow. Division A Division B Division C Sales $1,000,000 $ 300,000 $1,250,000 Less: Cost of goods sold Unit-level manufacturing costs Rent on manufacturing facility Gross margin Less: Operating expenses Unit-level selling and administrative expenses Division-level fixed selling and administrative (600,000) (135,000) 265,000 (200,000) (75,000) 25,000 (750,000) (100,000) 400,000 (62,500) (14,000)…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning